US prosecutors charge two dozen people over alleged $50m money laundering scheme.

Prosecutors in the United States have charged two dozen people over an alleged money laundering scheme involving Chinese shadow bankers and Mexico’s Sinaloa drug cartel.

Chinese underground money exchanges helped the cartel launder $50m in drug trafficking proceeds generated from the import of large amounts of fentanyl, cocaine, and methamphetamine between 2019 and 2023, the US Department of Justice (DOJ) said in a statement on Tuesday.

The California-based network then allegedly made the proceeds generated in the US accessible to cartel members in Mexico and elsewhere, the DOJ said.

Drug traffickers partnered with underground money exchanges to take advantage of the high demand for US dollars from Chinese citizens who use informal channels to move funds out of China, which bars annual transfers above $50,000, prosecutors said.

“The seller of US dollars provides identifying information for a bank account in China with instructions for the investor to deposit Chinese currency (renminbi) in that account. Once the owner of the account sees the deposit, an equivalent amount of US dollars is released to the buyer in the United States,” the DOJ said.

The 24 defendants face charges of conspiracy to distribute cocaine and methamphetamine and money laundering offences.

Law enforcement officials seized $5m in narcotics proceeds, 137kg of cocaine, 42kg of methamphetamine, and 3,000 ecstasy pills during the investigation, according to the DOJ.

“Relentless greed, the pursuit of money, is what drives the Mexican drug cartels that are responsible for the worst drug crisis in American history,” Drug Enforcement Administrator Anne Milgram said.

“Laundering drug money gives the Sinaloa cartel the means to produce and import their deadly poison into the United States,” Milgram added.

“DEA’s top operational priority is to save American lives by defeating the cartels and those that support their operations.”

China’s Ministry of Public Security said in a social media post on Wednesday it had also arrested a person suspected of involvement in “drug-related money laundering” following a US tip-off. “This case is a recent successful case of Sino-US anti-drug cooperation,” the ministry said on the social media platform Weibo.

Freezing hundreds of billions of dollars in lenders’ assets was part of dispute over gas project halted by sanctions.

A Russian court has ordered the seizure of the assets, accounts, property and shares of Deutsche Bank and Commerzbank in the country as part of a lawsuit involving the German banks, court documents showed.

The banks are among the guarantor lenders under a contract for the construction of a gas processing plant in Russia with the German company Linde. The project was terminated due to Western sanctions.

A court in St Petersburg ruled in favour of seizing 239 million euros ($260m) from Deutsche Bank, documents dated May 16 showed.

Deutsche Bank in Frankfurt said it had already provisioned about 260 million euros ($283m) for the case.

“We will need to see how this claim is implemented by the Russian courts and assess the immediate operational impact in Russia,” the bank added in a statement.

The court also seized the assets of Commerzbank, another German financial institution, worth 93.7 million euros ($101.85m) as well as securities and the bank’s building in central Moscow.

The bank is yet to comment on the case.

In a parallel lawsuit on Friday, the Russian court also ordered UniCredit’s assets, accounts and property, as well as shares in two subsidiaries, to be seized. The ruling covered 462.7 million euros ($503m) in assets.

UniCredit said it “has been made aware” of the decision and was “reviewing” the situation in detail. The bank was one of the most exposed European banks when Moscow launched its invasion of Ukraine, with a large local subsidiary operating in Russia.

It began preliminary discussions on a sale last year, but the talks have not advanced. Chief executive Andrea Orcel said UniCredit wants to leave Russia, but added that gifting an operation worth three billion euros ($3.3bn) was not a good way to respect the spirit of Western sanctions on Moscow over the conflict.

Russia has faced heavy Western sanctions, including on its banking sector, since the start of the war in Ukraine. Dozens of US and European companies have also stopped doing business in the country.

Revenues from Qatar’s LNG fields will provide budget surpluses until the 2030s, Fitch said.

Fitch Ratings has upgraded Qatar to AA, its third-highest rating, on the back of revenues expected from its expanded gas fields, the agency has said.

Revenues from Qatar’s liquified natural gas (LNG) fields will ensure that the country posts budget surpluses until the 2030s, Fitch said in a release on Wednesday outlining the rating rationale.

The upgrade from AA- “reflects Fitch’s greater confidence that debt to GDP will remain in line with or below the ‘AA’ peer median after falling sharply in recent years,” the agency said.

Fitch expects Qatar’s debt-to-GDP ratio to fall to about 47 percent of gross domestic product (GDP) in 2024 and 45 percent in 2025, from a peak of 85 percent in 2020.

Qatar is already one of the richest countries in the world and boasts one of the highest ratios of GDP per capita. The added revenue boost will ensure that its external balance sheet will strengthen from an already strong level, Fitch said.

However, Fitch warned that the continuing war in Gaza posed a risk to Qatar’s rating even though it had so far not been directly affected. Should a sharp escalation in regional tensions lead to capital flight from banks, for instance, or cause prolonged disruptions of Qatar’s hydrocarbon and transport sectors, that would affect the latest rating, Fitch said.

Qatar is one of the biggest exporters of LNG along with the United States, Australia and Russia. Asian countries led by China, Japan and South Korea have been the main market for Qatari gas, but demand has also grown from European countries since Russia’s war on Ukraine threw supplies into doubt.

Qatar Energy plans to expand LNG production capacity at North Field from 77 million tonnes per year (mtpa) to 110 mtpa by end-2025, 126 mtpa by end-2027 and announced a further expansion to 142 mtpa by end-2030.

The North Field is part of the world’s largest gas field, which Qatar shares with Iran, which calls its share South Pars.

Competition for LNG has ramped up since the start of the war in Ukraine, with Europe, in particular, requiring a large quantity to help replace Russian pipeline gas that used to make up almost 40 percent of the continent’s imports.

However, after a decade of meteoric price rise, gas prices dropped earlier this year to nearly all-time lows after adjusting for inflation. Despite that drop, all leading gas producers, including the US, Australia and Russia, want to increase output betting on further demand growth.

New York City – Rachel S lives in a walkable neighbourhood in Brooklyn, New York. Most days she is able to live comfortably without a car. She works remotely often but occasionally she needs to go into the office. That’s where her situation gets a bit challenging. Her workspace is not easily accessible by public transportation.

Because she doesn’t need to drive often she applied for the car-sharing platform Zipcar to fulfill her occasional need. The application process is pretty fast allowing consumers to get on the road using its fleet of cars relatively quickly.

Unfortunately, that was not the case for Rachel. As soon as she pressed the submit button she was deemed ineligible by the artificial intelligence software the company uses. Puzzled about the outcome, Rachel got in touch with the company’s customer service team.

After all, she has no demerits that would suggest she’s an irresponsible driver. She has no points on her licence. The only flump was a traffic ticket she received when she was seventeen years old and that citation was paid off years ago.

Although the traffic citation has since been rectified, now in her thirties she is still dealing with the consequences.

She talked to Zipcar’s customer service team to no avail. Despite an otherwise clean driving record, she was rejected. She claims that the company said she had no recourse and that the decision could not be overwritten by a human.

“There was no path or process to appeal to a human being and while it is reasonable the only way to try again would be to reapply” for which there is a nonrefundable application fee, Rachel told Al Jazeera recalling her conversation with the company.

Zipcar did not respond to Al Jazeera’s request for comment.

Rachel is one of the many consumers who were declined loans, memberships and even job opportunities by AI systems without any recourse or appeal policy as companies continue to rely on AI to make key decisions that impact everyday life.

That includes D who recently lost their job.

As a condition of the interview D requested that we only use their initial out of respect for their privacy. D searched religiously for a new opportunity to no avail.

After months of looking, D finally landed a job but there was one huge problem — the timing.

It was still several weeks before D started the new job and it was several weeks after that D received the first paycheck.

To get some extra help, D applied for a personal loan on multiple platforms in an effort to circumvent predatory payday loans, just to get by in the meantime.

D was rejected for all the loans they applied for. Although D did not confirm which specific firms, the sector has multiple options including Upstart, Upgrade, SoFi, Best Egg and Happy Money, among others.

D says when they called the companies after submitting an online application, no one could help nor were there any appeals.

When D was in their early twenties they had a credit card which they failed to pay bills on. That was their only credit card. They also rent an apartment and rely on public transportation.

According to online lenders driven by AI, their lack of credit history and collateral makes them ineligible for a loan despite paying off their outstanding debt six years ago.

D did not confirm which specific companies they tried for a loan. Al Jazeera reached out to each of those companies for comment on their processes — only two responded — Upgrade and Upstart — responded by the time of publication.

“There are instances where we’re able to change the decision on the loan based on additional information, i.e. proof of other sources of income, that wasn’t provided in the original application, but when it comes to a ‘human judgment call,’ there is a lot of room for personal bias which is something regulators and industry leaders have worked hard to remove,” an Upgrade company spokesperson said in an email to Al Jazeera. “Technology has brought objectivity and fairness to the lending process, with decisions now being made based on the applicant’s true merit.”

Historical biases amplified

But it isn’t as simple as that. Existing historical biases are often amplified with modern technology. According to a 2021 investigation by the outlet The Markup, Black Americans are 80 percent more likely to be auto-rejected by loan granting agencies than their white counterparts.

“AI is just a model that is trained on historical data,” said Naeem Siddiqi, senior advisor at SAS, a global AI and data company, where he advises banks on credit risk.

That’s fueled by the United States’ long history of discriminatory practices in banking towards communities of colour.

“If you take biased data, all AI or any model will do is essentially repeat what you fed it,” Siddiqui said.

“The system is designed to make as many decisions as possible with as less bias and human judgment as possible to make it an objective decision. This is the irony of the situation… of course, there are some that fall through the cracks,” Siddiqi added.

It’s not just on the basis of race. Companies like Apple and Goldman Sachs have even been accused of systemically granting lower credit limits to women over men.

These concerns are generational as well. Siddiqi says such denials also overwhelmingly limit social mobility amongst younger generations, like younger millennials (those born between 1981 and 1996) and Gen Z (those born between 1997 and 2012), across all demographic groups.

That’s because the standard moniker of strong financial health – including credit cards, homes and cars – when assessing someone’s financial responsibility is becoming increasingly less and less relevant. Only about half of Gen Z have credit cards. That’s a decline from all generations prior.

Gen Zers are also less likely to have collateral like a car to wager when applying for a loan. According to a recent study by McKinsey, the age group is less likely to choose to get a driver’s licence than the generations prior. Only a quarter of 16-year-olds and 45 percent of 17-year-olds hold driving licences. That’s down 18 percent and 17 percent, respectively.

The Consumer Financial Protection Bureau has stepped up its safeguards for consumers. In September, the agency announced that credit lending agencies will now need to explain the reasoning behind a loan denial.

“Creditors often feed these complex algorithms with large datasets, sometimes including data that may be harvested from consumer surveillance. As a result, a consumer may be denied credit for reasons they may not consider particularly relevant to their finances,” the agency said in a release.

However, the agency does not address the lack of a human appeal process as D claims to have dealt with personally.

D said they had to postpone paying some bills which will hurt their long-term financial health and could impact their ability to get a loan with reasonable interest rates, if at all, in the future.

‘Left out from opportunities’

Siddiqi suggests that lenders should start to consider alternative data when making a decision on loans which can include rent and utility payments and even social media behavior as well as spending patterns.

On social media foreign check-ins are a key indicator.

“If you have more money, you tend to travel more or if you follow pages like Bloomberg, the Financial Times, and Reuters you are more likely to be financially responsible,” Siddiqi adds.

The auto-rejection problem is not just an issue for loan and membership applications, it’s also job opportunities. Across social media platforms like Reddit users post rejection emails they get immediately upon submitting an application.

“I fit all the requirements and hit all the keywords and within a minute of submitting my application, I got both the acknowledgement of the application and the rejection letter,” Matthew Mullen, the original poster, told Al Jazeera.

The Connecticut-based video editor says this was a first for him. Experts like Lakia Elam, head of the Human Resources consulting firm Magnificent Differences Consulting says between applicant tracking systems and other AI-driven tools, this is increasingly becoming a bigger theme and increasingly problematic.

Applicant tracking systems often overlook transferable skills that may not always align on paper with a candidate’s skill set.

“Often times applicants who have a non-linear career path, many of which come from diverse backgrounds, are left out from opportunities,” Elam told Al Jazeera.

“I keep telling organisations that we got to keep the human touch in this process,” Elam said.

But increasingly organisations are relying more on programs like ATS and ChatGPT. Elam argues that leaves out many worthwhile job applicants including herself.

“If I had to go through an AI system today, I guarantee I would be rejected,” Elam said.

She has a GED—- the high school diploma equivalency — as opposed to a four-year degree.

“They see GED on my resume and say we got to stay away from this,” Elam added.

In part, that’s why Americans do not want AI involved in the hiring process. According to an April 2023 report from Pew Research, 41 percent of Americans believe that AI should not be used to review job applications.

“It’s part of a larger conversation about losing paths to due process,” Rachel said.

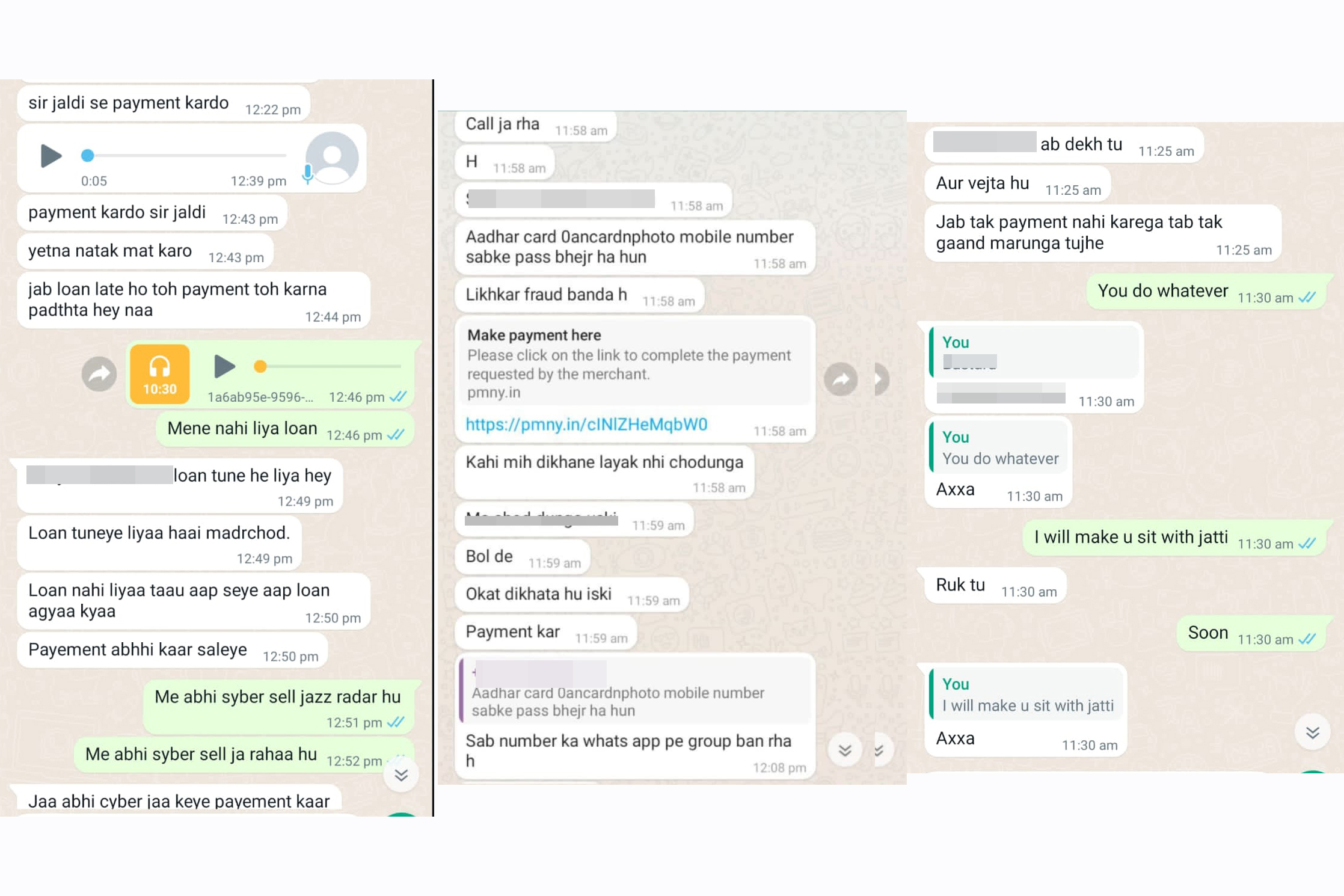

On August 12, a family in the central Indian city of Bhopal took a selfie in their home. After the photo, the father, Bhupendra Vishwakarma, gave his two sons, eight and three years old, a poisoned drink, and he and his wife took their lives by hanging themselves.

In his four-page suicide note, Vishwakarma, 35, who worked in an insurance firm, wrote that he was trapped in a cycle of debt from loan apps. Recovery agents had been tormenting him for months and the last message he received from them tipped him over the edge.

It said, “Tell him to repay the loan; otherwise, today I will strip him naked and upload it on social media.”

In his suicide note, Vishwakarma said, “Today, the situation has reached the point of losing my job as well. I can’t see a future for myself and my family. I am no longer worthy of showing my face to anyone. How will I face my family?”

Police have arrested five people involved in the scam so far even as the investigation continues.

Vishwakarma’s story is not unique. Shivani Rawat, a 23-year-old college receptionist in Delhi, faced her own ordeal. In June 2023, she applied for a 4,000 rupee ($48) loan through an app called “Kreditbe”, since her salary was delayed. Her loan request remained pending, with no funds received. Yet, within a week, she began receiving 10-15 calls demanding 9,000 rupees ($108) for repayment.

Rawat said she told the recovery agents that she hadn’t received any money in her account, “but they started using abusive language. When I stopped answering their calls, they began sending me abusive texts.”

In August, her colleagues received manipulated explicit photos of her and her family that had been sent by representatives of Kreditbe. She tried to explain the situation to her coworkers, but the next day, her manager asked her to resign because her presence made others uncomfortable.

“After losing my job, I became so depressed that I even had thoughts of ending my life,” Rawat admitted.

Al Jazeera tried reaching out to Kreditbe for a comment but there was no information available on the firm and none of the representatives who had been in touch with Rawat were available any more.

Bhupendra Vishwakarma took a selfie with his family before he died by suicide [Anil Kumar Tyagi/Al Jazeera]

Kreditbe’s name is a rip-off of a legitimate loan app called KreditBee, a common modus operandi for these illegal loan apps which often choose names similar to reputable brands to create a sense of authenticity.

Both Vishwakarma and Rawat had borrowed money from lending apps, which offer loans to users in a convenient, few clicks and without the extensive documentation that a traditional bank loan requires. The money is credited to the borrower’s account within a few minutes, unlike the five to seven days that a bank loan takes for borrowers who meet the high eligibility bar.

These apps saw a rise in use during the pandemic as with many businesses shut or scaled back, a significant number of people were unemployed and in financial difficulties.

The average loan tickets in these apps range between 10,000 rupees to 25,000 rupees ($120 to $300) with monthly interest rates of 20 percent to 30 percent and a processing fee that can be as much as 15 percent.

Loan app representatives typically begin the recovery process 15 days after approving the loan. However, in many cases, they have been known to start harassing people just four to six days after disbursing the loan, and in Tiwari’s case, it was even before she actually received the loan.

As per Akshay Bajpai, an independent cybersecurity expert in Bhopal, currently, more than 700 loan apps are operating in the country, some of which are Indian but the majority of which are Chinese-owned and hire Indians to run them.

While some of them are outright frauds and use the promise of quick money to get fees from desperate loan seekers before disappearing in the night, others are in a grey area not just because of the malicious methods they employ to extort money from innocent people but also because they don’t follow the central bank rules on online lending including on the annual interest rate, various charges.

The Reserve Bank of India (RBI) has also clearly said that no lending institution can store customer details except some minimal data such as the name, address and contact details of the customer. However, illegal apps access contact lists and pictures, edit them and use manipulated images to blackmail borrowers to recover money.

According to a study conducted by CloudSek, a cybersecurity software company, between July 22, 2023, and September 18, 2023, their experts monitored 55 fraudulent loan apps that targeted individuals. Additionally, they identified more than 15 obscure payment gateways operated by individuals of Chinese origin who undertook those steps to evade detection.

The Chinese loan apps also employ this modus operandi in Southeast Asia and some African nations, as well. In countries where people are less aware of cybersecurity and fraud, people become easy targets for such malicious activities.

Creating fear

Loan apps representatives harass borrowers with threatening and abusive messages and calls like these that Shivani Rawat received [Courtesy Shivani Rawat]

“Scammers instil fear in the minds of their victims by employing various tactics. Initially, they may threaten to access the victim’s contact list and make calls. If the victim resists, they may infiltrate the victim’s photo gallery, manipulate images, and send them back,” explained Pravin Kalaiselvan, founder of SaveThem India, an NGO that spreads awareness about cybercrime.

“This induces panic among the victims, ultimately leading them to comply with the scammers’ demands for money,” he added.

In the last three years, Loan Consumer Association (LCA), a group of advocates and social workers focused on combating unethical recovery practices by banks and apps, has helped almost 1,800 people stuck in these illegal loan app traps both with counselling and help them file complaints with the police.

According to Nikkhil Jethwa, a cyber-safety expert and founder of LCA, nearly 90 percent of these individuals were dealing with clinical depression and distress. Some would even panic or start shivering when their phones rang, he recalled.

Escalating complaints

Complaints about digital lending have surged since Prime Minister Narendra Modi put the country in lockdown in March 2020 in the early days of the COVID-19 pandemic, according to data from SaveThem India Foundation.

That year, the foundation received approximately 29,000 complaints filled with horror stories of intimidating calls and messages from the representatives of the loan apps. That number went up to about 76,000 in 2021. They have received 46,359 complaints in the first nine months of this year.

According to a survey conducted by LocalCircle from July 2020 to June 2022, 14 percent of surveyed Indians utilised instant loan applications in the past two years. Fifty-eight percent encountered exorbitant interest rates of 25 percent and 54 percent of the respondents reported experiencing incidents of extortion or data misuse during the collection process.

‘Government agencies unprepared’

In his suicide note, Vishwakarma wrote that he visited the Cyber Crime Office in Bhopal but received no assistance from the officers.

A senior police official from Madhya Pradesh who declined to be named as he is not authorised to speak to the media told Al Jazeera that the police was just not trained to deal with cybercrime.

“Many policemen in cyber-police stations lack even basic internet knowledge, while cybercriminals are well-equipped with the latest technology. This is why most cybercrimes go unsolved,” he said.

Indian police are not trained to deal with cybercrime [File: Ajit Solanki/AP Photo]

Interactive Voice Response is another tool used by scammers as companies that offer this service provide it without strict documentation. It’s used to target people who are not active online on sites like Facebook, where loan apps usually advertise their apps, said Kalaiselvan.

A majority of these scammers use virtual numbers from neighbouring countries like Bangladesh, Pakistan, and Nepal, making it challenging to track them down.

“Loan scammers take advantage of these services, making it hard for authorities to catch them,” Kalaiselvan said.

According to experts, these apps typically have names that include keywords like “easy”, “loan”, “Aadhar” and “emi”, making them easily discoverable through online searches (Aadhar is the unique 12-digit ID that people in India need to avail banking services).

Additionally, they promote their services on platforms, such as Facebook, and on Google via its AdSense which allows website owners to display targeted ads to expand their user base. When these apps face bans or complaints, they often alter their names and other details, reemerging with a new identity.

Loan app scammers extort money through bank accounts, but despite the availability of that record, very few scammers are apprehended, said Jethwa.

One reason is that very few Indians are digitally savvy. According to Oxfam’s India Inequality Report 2022, just 38 percent of households in the country possess digital literacy.

“The government promotes Digital India, but we lack the infrastructure and cyber-literacy programmes for the people,” said Jethwa.

Measures taken

In March, the Directorate of Enforcement (ED) seized moveable assets worth 1.06 billion rupees ($12.76m) in Bengaluru in connection with financial frauds committed by Chinese loan apps.

The ED stated that these companies swiftly offered short-term loans to the public via loan apps and other channels, imposing steep processing fees along with excessively high interest rates. They recovered amounts from the borrowers through coercive tactics, including relentless phone threats and causing emotional distress.

In a report, Google India said it removed more than 3,500 personal loan applications from its Play Store in 2022 due to their failure to comply with its policies and regulations. These apps were unlawfully accessing user data, including contacts and photos.

In September 2022, India’s Finance Minister Nirmala Sitharaman said that the RBI would make a list of legal apps, and the Ministry of Electronics and Information Technology (MeitY) would ensure only these approved apps were available on Google Play Store and Apple App Store.

On February 7, 2023, in response to a parliamentary question, the Finance Ministry said that it has forwarded a whitelist of approved digital lending apps to app stores such as Google Play Store and Apple App Store. However, that statement was debunked by local media which reported no such list had been sent.

Around the same time, central bank governor Shaktikanta Das said that digital lending apps are not under the regulatory purview of the central bank.

That same month the government banned 94 lending apps, which included names like BuddyLoan, CashTM, Indiabulls Home Loans, PayMe, Faircent, and RupeeRedee. These apps had been flagged by the RBI for various reasons, and many of them had either Chinese investors or had been involved in harassing borrowers.

ZURICH – Credit Suisse is expected to face shareholder anger at what will be its final annual general meeting on Tuesday after the bank was rescued last month by rival UBS.

The hastily arranged takeover by Zurich-based UBS, for which Switzerland invoked emergency legislation, bypassed Credit Suisse shareholders, who would otherwise have had a say, and largely wiped out the value of their holdings.

The meeting marks an ignominious end for the 167-year-old flagship bank founded by Alfred Escher, a Swiss magnate affectionately dubbed King Alfred I, who helped build the country’s railways and then the bank.

Protesters gathered outside the concert venue where the meeting was taking place, with some erecting a capsized boat to depict the bank’s demise.

Shareholder advisory firm Ethos decried the “greed and incompetence of its managers” as well as pay that reached “unimaginable heights”, as it prepared to challenge top executives at the meeting.

AFP via Getty Images

“Shareholders have lost considerable amounts of money and thousands of jobs are on the line,” it said.

After years of scandal and losses, Credit Suisse came to the brink of collapse before UBS rode to the rescue with a merger engineered and bankrolled by the Swiss authorities.

The meeting is the first time that Chairman Axel Lehmann and Chief Executive Ulrich Koerner will publicly address shareholders since the takeover was announced.

Credit Suisse had been attempting to put the past behind it and restructure, before a shock triggered by the collapse of Silicon Valley Bank in the U.S. sent it into a spiral.

Credit Suisse came to the brink of collapse before UBS rode to the rescue with a merger engineered and bankrolled by the Swiss authorities.Getty Images

After a run on deposits, the Swiss government turned to UBS, which agreed to buy Credit Suisse for $3.3 billion, a fraction of its earlier market value.

The move angered not only shareholders but many in Switzerland.

A recent survey by political research firm gfs.bern found a majority of Swiss did not support the deal.

“The government’s use of emergency powers to push this deal through goes beyond legal and democratic norms,” said Dominik Gross of the Swiss Alliance of Development Organizations.

The Swiss government turned to UBS, which agreed to buy Credit Suisse for $3.3 billion. AFP via Getty Images

“Swiss taxpayers too are on the hook for billions of francs of junk investments and yet the government, FINMA and the central bank have given little explanation about the state’s 9 billion (franc) loss guarantee to UBS.”

One of the world’s biggest investors, Norway’s sovereign wealth fund said it would vote against the re-election of Lehmann and six other directors, in a public show of protest.

U.S. proxy adviser Institutional Shareholder Services (ISS) had earlier rebuked the bank’s management for a “lack of oversight and poor stewardship”.

In the lead-up to Tuesday’s meeting, Credit Suisse said it had withdrawn certain proposals from the agenda.

Those include the discharge of management, which is typically a bellwether of confidence. It also ditched plans for a special bonus linked to the bank’s transformation plan.

Credit Suisse’s near collapse also completely wiped out $17 billion of Additional Tier 1 (AT1) debt.

A group of AT1 investors has hired law firm Quinn Emanuel Urquhart & Sullivan to demand compensation.

Meanwhile, the office of the attorney general on Sunday said Switzerland’s Federal Prosecutor has opened an investigation into the Credit Suisse takeover.

The prosecutor is looking into potential breaches of Swiss criminal law by government officials, regulators and executives at the two banks.

Credit Suisse and UBS shares fell on Monday after Switzerland’s federal prosecutor opened an investigation into the emergency merger of the two lenders.

The office of the attorney general said on Sunday that the prosecutor opened an investigation into the state-backed takeover of Credit Suisse by UBS Group last month, looking into potential breaches of the country’s criminal law by government officials, regulators and executives at the two banks.

UBS and Credit Suisse were each set for their biggest daily decline in 10 days, falling around 4% in early trading before paring losses to stay down 2% and 1.8%, respectively.

The banks declined to comment on the investigation.

The UBS takeover of rival Credit Suisse was engineered by Swiss authorities in a bid to rein in turmoil in global banking.

The UBS takeover of rival Credit Suisse was engineered by Swiss authorities in a bid to rein in turmoil in global banking.AP

“The government underestimated how much antipathy the public in Switzerland have against the deal,” said Michael Field, Europe Market Strategist at Morningstar.

“Comments in the media this morning about 30% of workforce being cut don’t help either,” he added.

Swiss daily Tages-Anzeiger reported on Sunday, citing an unnamed senior UBS manager that the bank created by takeover of Credit Suisse is poised to reduce its workforce by 20-30%. The two banks combined have 120,000 staff worldwide and $1.6 trillion in assets.

Separately, data showed on Monday that sight deposits held by the SNB declined last week, suggesting that Credit Suisse and UBS may have cut back on use of emergency funds offered them.

The SNB, Credit Suisse and UBS declined to comment on the changes in sight deposits.

The boss of the Saudi National Bank abruptly resigned from his post Monday, just days after his critical comments about Credit Suisse sparked an industrywide panic that resulted in a forced rescue of the troubled lender by rival UBS.

Saudi National Bank Chairman Ammar Al Khudairy is stepping down “due to personal reasons,” a press release said without further elaboration.

He had led the bank since 2021.

Mohammed Al Ghamdi will replace Al Khudairy as chairman.

Al Khudairy’s resignation came less than two weeks after he rattled the market about Credit Suisse, whose troubles had reignited fears of a global banking meltdown.

“The SNB Chairman was a victim of giving his honest opinion at such a tense time for Credit Suisse,” Mohammed Ali Yasin, a capital markets specialist and investment advisor, told Bloomberg.

Ammar Al Khudairy had led the Saudi National Bank since 2021.Bloomberg

The outgoing chairman had declared during a Bloomberg Television appearance that the Saudi National Bank, Credit Suisse’s biggest shareholder, would not consider pouring more money into the Swiss banking giant.

“The answer is absolutely not, for many reasons outside the simplest reason, which is regulatory and statutory,” Al Khudairy said in the March 15 interview.

Al Khudairy later attempted to do damage control, telling CNBC that the panic over Credit Suisse’s potential failure was “completely unwarranted.”

Nevertheless, Credit Suisse shares plunged to record lows following Al Khudairy’s remarks.

The bank had faced a crisis of confidence among investors after top executives admitted to “material weaknesses” in its financial reporting practices over the last two years.

“In hindsight, seeing the buyout rate of CS by UBS, his answer was the right course of action: awaiting for the crisis to be clearer.”

Ammar Al Khudairy’s remarks prompted a major selloff of Credit Suisse shares.REUTERS

The Saudi National Bank is the largest commercial bank in Saudi Arabia. It formed after a merger of National Commercial Bank and Samba Financial Group.

The Credit Suisse crisis culminated in a government-brokered emergency rescue in which its Swiss banking rival UBS agreed to a $3.3 billion takeover.

The deal helped to assuage concerns among investors about the overall health of the global banking system, though it was expected to result in tens of thousands of layoffs.

UBS reached a takeover deal for Credit Suisse last week.AFP via Getty Images

Credit Suisse is one of several banks under close scrutiny after the collapses of Silicon Valley Bank and Signature Bank of New York prompted concerns about a global contagion event.

It’s a funny but sad spectacle that Joe Biden & Co. are trying to turn the mess at Silicon Valley Bank — and the crisis engulfing the banking system — into a political win.

Funny because the BS is working about as well as their spinning of the transitory nature of inflation, or how well they handled the alarmingly chaotic pullout from Afghanistan.

Of course, the final word has yet to be written on the collapse of SVB, Signature Bank, the near-collapse of First Republic Bank, and whatever else implodes by the time this column is in the paper.

But one thing I know for sure is that banking crises demand leadership from Washington — stuff that’s so obviously lacking at a time when it’s so desperately needed.

Back in 2008 we had Treasury Secretary Hank Paulson working day and night putting out multiple fires and leveling with Congress and the American people about the severity of the situation. Today we have Sleepy Joe Biden, his equally asleep Treasury Secretary Janet Yellen announcing that bank bailouts aren’t really bailouts because taxpayers aren’t involved.

Really?

Treasury Secretary Janet Yellen reportedly said that bank bailouts aren’t really bailouts because taxpayers aren’t involved.AFP via Getty Images

The government just handed SVB a blank check to cover all its depositors, mainly lefty Bay Area venture capitalists. That means all accounts are covered with FDIC insurance, even those above the limit of $250,000.

He says with a straight face the money is coming from the big banks who contribute to the FDIC insurance pool. OK, but if the banks are financing the fund, they will pass on those costs to depositors. That means everyone with a bank account, which means just about every American taxpayer, will be making whole those wealthy VC dudes.

Duh.

Not very ‘stress’ful

Biden and Yellen then say the watering down of the banking law known as Dodd-Frank meant that midsized banks like SVB were spared the so-called stress tests that would have uncovered its weaknesses. They appear to ignore (or most likely have no clue) the dirty little secret that such exams are known derisively in banking circles as “feather tests” because even big risk-management-challenged basket cases like Citigroup seem to pass them.

Another whopper: Biden and Yellen want us to believe that the San Francisco Fed had no idea what was happening in its backyard with a bank that grew exponentially in three years before it sank.

Again, don’t believe it. SVB’s CEO was on the board of his local Fed bank. Everyone who should have known what SVB was up to did. And by many accounts they were too busy making sure the banks they regulated lived up to ESG standards and embraced so-called social-justice remedies to care about SVB’s obvious risk taking. One of my sources worked at SVB until about a year ago, and here’s how he described the bank’s business model: “Loans to VC-backed companies that made no money, asset-based credit lines to PE funds and little else. It should never have been given FDIC insurance. This wasn’t a place that made loans to construction companies and took deposits from your aunt.”

Biden said the watering down of Dodd-Frank meant that SVB were spared the so-called stress tests that would have uncovered its weaknesses. Bloomberg via Getty Images

Yes, FDIC insurance was supposed to protect smallish depositors like your aunt, not dice-rolling tech millionaires who banked at SVB and knew it was a risky business. Those tech millionaires (like the SF Fed) either knew or should have known that a hiccup in the economy like rising rates could doom this bank and maybe others.

As I first reported last week, the big banks are now freaking out about another midsized bank also in San Francisco about to succumb to market forces named First Republic. (See a pattern here?) They chipped in with $30 billion to stabilize the bank at least for the time being.

Stay On the Money

Essential weekly read to fuel business lunches.

That’s because I also hear the bank could be sold in the coming days to one of the bailout participants. The reason they’re doing this is not necessarily because they think First Republic is a great business — rather they’re seriously worried about economic contagion that policy makers have no clue how to handle.

Remember 2008?

The bill is coming due for the unserious economic policies of the past two-plus years: The wildly unprecedented spending by the Biden administration to turn the US into a quasi-socialist European welfare state and money printing by the Fed to make that happen.

Every top bank executive I speak to says the current troubles in the financial system could lead to something on the scale of what went down in 2008. They’re also seriously worried the banking tumult is yet another example of Sleepy Joe & Co. not being up for the job.

Or as one remarked to me: “Where’s Hank Paulson when you need him?”

Credit Suisse on Thursday said it would borrow up to $54 billion from the Swiss central bank to shore up liquidity and investor confidence after a slump in its shares intensified fears about a global financial crisis.

The Swiss bank’s announcement helped stem heavy selling in financial markets in Asian morning trade on Thursday, following torrid sessions in Europe and the United States overnight as investors fretted about potential runs on global bank deposits.

In its statement early Thursday, Credit Suisse said it would exercise an option to borrow from the central bank up to 54 billion dollars. That followed assurances from Swiss authorities on Wednesday that Credit Suisse met “the capital and liquidity requirements imposed on systemically important banks” and that it could access central bank liquidity if needed.

The Credit Suisse logo on one of the buildings at the North Carolina campus on March 15, 2023.REUTERS

Credit Suisse is the first major global bank to be given an emergency lifeline since the 2008 financial crisis and its problems have raised serious doubts over whether central banks will be able to sustain their fight against inflation with aggressive interest rate hikes.

Asian stocks followed Wall Street’s tumble on Thursday and investors bought gold, bonds and the dollar. While the bank’s announcement helped trim some of those losses, trade was volatile and sentiment fragile.

“It does help. It removes an immediate risk. But it confronts us with another choice. The more we do this, the more we blunt monetary policy, the more we have to live with higher inflation — and what is it going to be?” said Damien Boey, chief equity strategist at Barrenjoey in Sydney.

“Do bailouts make things better? On the one hand, you are removing a source of risk to the markets which is a clear and present danger. On the other hand we are feeding into this paradigm of monetary policy bucking within itself.”

Credit Suisse’s borrowing will be made under the covered loan facility and a short-term liquidity facility, fully collateralised by high quality assets. It also announced offers for senior debt securities for cash of up to 3.2 billion dollars.

“This additional liquidity would support Credit Suisse’s core businesses and clients as Credit Suisse takes the necessary steps to create a simpler and more focused bank built around client needs,” the bank said.

Credit Suisse Chief Executive Ulrich Koerner had earlier on Wednesday sought to reassure investors about the lender’s strong liquidity.

“Our capital, our liquidity basis is very, very strong,” Koerner told media. “We fulfill and overshoot basically all regulatory requirements.”

Credit Suisse Group AG, CEO Ulrich Koerner at an interview in London on March 14, 2023Bloomberg via Getty Images

EUROPEAN EPICENTER

The 167-year-old bank’s problems have shifted the focus for investors and regulators from the United States to Europe, where Credit Suisse led a selloff in bank shares after its largest investor said it could not provide more financial assistance because of regulatory constraints.

Investor focus is also on any action by central banks and other regulators elsewhere to restore confidence in the banking system as well as any exposure businesses may have to Credit Suisse.

Silicon Valley Bank’s demise last week, followed by that of Signature Bank two days later, sent global bank stocks on a roller-coaster ride this week, with investors discounting assurances from U.S. President Joe Biden and emergency steps giving banks access to more funding.

On Wednesday, Credit Suisse shares led a 7% fall in the European banking index, while five-year credit default swaps for the flagship Swiss bank hit a new record high.

The investor exit for the doors raised fears of a broader threat to the financial system, and two supervisory sources told Reuters that the European Central Bank had contacted banks on its watch to quiz them about their exposures to Credit Suisse.

The U.S. Treasury also said it is monitoring the situation around Credit Suisse and is in touch with global counterparts, a Treasury spokesperson said.

‘FLIGHT TO SAFETY’

Rapid rises in interest rates have made it harder for some businesses to pay back or service loans, increasing the chances of losses for lenders who are also worried about a recession.

Traders are now betting that the Federal Reserve, which just last week was expected to accelerate its interest-rate-hike campaign in the face of persistent inflation, may be forced to hit pause and even reverse course.

Bets on a large European Central Bank interest-rate hike at Thursday’s meeting also evaporated quickly on growing fears about the health of Europe’s banking sector. Money market pricing suggested traders now saw less than a 20% chance of a 50 basis point rate hike at the ECB meeting.

The Credit Suisse campus in Research Triangle Park in Morrisville, North Carolina. REUTERS

Unease sparked by SVB’s demise has also prompted depositors to seek out new homes for their cash.

Ralph Hammers, CEO of Credit Suisse rival UBS said market turmoil has steered more money its way and Deutsche Bank CEO Christian Sewing said that the German lender has also seen incoming deposits.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.