Opinion by Alexander Kozul-Wright, Ruurd Brouwer (geneva)

Inter Press Service

The International Monetary Fund (IMF) and the World Bank share a common goal of raising living standards in their member countries. This week, the two international institutions will convene in Washington DC (through October 16) for their annual meeting. The strength of the US dollar will be a key talking point. By adjusting their lending practices, these institutions have a unique opportunity to relieve suffering in the world’s poorest countries.

GENEVA, Oct 11 (IPS) – In the last week of September, emerging market (EM) bond fund outflows hit $4.2 billion, according to JP Morgan, bringing this year’s total to a record $70 billion. The exodus, set off by a rising U.S. dollar, is heaping pressure on low-income countries.

The greenback’s rise has been fuelled by interest-rate hikes by the Federal Reserve. Since March, the Fed has raised rates by three percentage points, prompting global investors to move their funds into U.S. financial assets and away from (riskier) EM investments.

While economists continue to wrangle over their U.S. growth forecasts, this ‘flight to quality’ has sent financial shockwaves across the developing world, already straining under elevated costs for food and fuel – typically priced in U.S. dollars. Moreover, attempts by EM policy makers to stem the dollar’s rise have largely failed.

Over the course of this year, central banks around the world have drained their U.S. dollar reserves at the fastest rate since 2008. To stem currency depreciations, they have also raised interest rates aggressively. In Argentina, for instance, policy makers raised rates to 75% last month. To little avail.

The MSCI Emerging Market Currency Index, which measures the total return of 25 emerging market currencies against the U.S. Dollar, is down nearly 9 percent from January 1st. The Egyptian pound has depreciated by 20% over the same period, according to Bloomberg data. In Ghana, the Cedi has fallen by 41%.

On top of higher imports costs, a plunging currency makes the servicing of dollar- denominated debt more expensive. This concern may seem abstract to people in advanced economies. In developing nations, however, the effects are painfully real.

As the dollar appreciates relative to other currencies, more domestic currency (in the form of tax revenues) has to be generated to service existing dollar debts. For low-income governments, budget cuts have to be implemented in the hope of avoiding sovereign default.

Currency depreciations have the power to strongarm authorities into reducing health and education spending, just to stay current on their debts. This leaves officials with a grim choice: either risk unleashing a full-blown debt crisis, or confiscate essential public services.

Given the painful costs of insolvency, governments tend to prioritize austerity over bankruptcy. Together with the oft-publicized effects of lost access to foreign investment, subdued growth and high unemployment, sovereign default also imposes severe social tolls.

In August, the World Bank published a paper measuring the decline in country living standards – looking at access to food, energy and healthcare – after state bankruptcies. The paper showed that ten years after default, countries experience 13% more infant deaths per year, on average, compared to the synthetic control (counterfactual) group.

Admittedly, more developed emerging markets like Brazil and India can issue bonds in their own currency to limit budget cutbacks. In most of the world’s poor countries, however, financial markets are too shallow to support domestic lending.

With no recourse to borrow from private creditors, public bodies like multi-lateral development banks (MDBs) usually step in to fill the gap. Indeed, almost 90% of low-income countries’ (LICs) funding takes the form of concessional, or non-commercial, loans from official lenders.

Even accounting for these favourable terms, financial pressures are beginning to build outside of well-known hot spots like Lebanon, Sri Lanka and Pakistan. As it stands, LICs have outstanding debts to MDBs and other official creditors to the tune of $153 billion (mostly denominated in USD).

Given the exogenous trigger for capital outflows from developing countries this year, multi-lateral lenders need to be more innovative. Where possible, they should use their robust credit ratings to assume greater risk by lending to poor countries in domestic currencies.

Failing that, they could lend in synthetic local currencies. These instruments index dollar debts to local exchange rates, allowing borrowers to service liabilities in their own currency while ensuring that creditors receive payments (both interest and principal) in dollars.

Synthetic currencies can improve debtor credit profiles by limiting foreign capital outflows and, by extension, improve debt management capacity. In particular, they boost economic resiliency by making government finances less a function of international currency volatility.

Multilateral financial institutions have been tasked with designing a stable international monetary system to try and ease global poverty. But the loans provided by these groups undermine their own mission, as dollar debts force currency risk onto the countries least able to handle it.

This week, the World Bank and the IMF will convene in Washington (October 10-16) for their annual meeting. The strength of the USD will be a key talking point. By adjusting their lending practices, these institutions have a unique opportunity to relieve suffering in the world’s poorest countries.

Alexander Kozul-Wright is a researcher at Third World Network and Ruurd Brouwer is Chief Executive Officer at TCX, a currency hedging firm (https://www.tcxfund.com).

Opinion by Jomo Kwame Sundaram, Anis Chowdhury (sydney and kuala lumpur)

Inter Press Service

SYDNEY and KUALA LUMPUR, Oct 10 (IPS) – The dogmatic obsession with and focus on fighting inflation in rich countries are pushing the world economy into recession, with many dire consequences, especially for poorer countries. This phobia is due to myths shared by most central bankers.

Anis Chowdhury

Myth 1: Inflation chokes growth

The common narrative is that inflation hurts growth. Major central banks (CBs), the Bretton Woods institutions (BWIs) and the Bank of International Settlements (BIS) all insist inflation harms growth despite all evidence to the contrary. The myth is based on a few, very exceptional cases.

“Once-in-a-generation inflation in the US and Europe could choke off global growth, with a global recession possible in 2023”, claimed the World Economic Forum Chief Economist’s Outlook under the headline, “Inflation Will Lead Inexorably To Recession”.

The Atlantic recently warned, “Inflation Is Bad… raising the prospect of a period of economic stagnation or even a recession”. The Economist claims, “It hurts investment and makes most people poorer”.

Jomo Kwame Sundaram

Without evidence, the narrative claims causation runs from inflation to growth, with inevitable “adverse” consequences. But serious economists have found no conclusive supporting evidence.

World Bank chief economist Michael Bruno and William Easterly asked, “Is inflation harmful to growth?” With data from 31 countries for 1961-94, they concluded, “The ratio of fervent beliefs to tangible evidence seems unusually high on this topic, despite extensive previous research”.

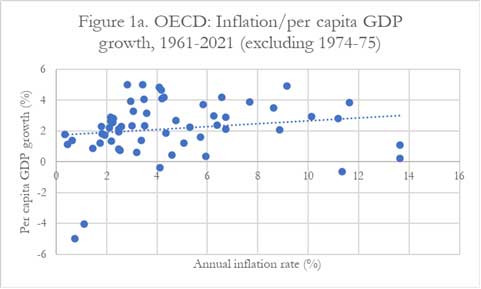

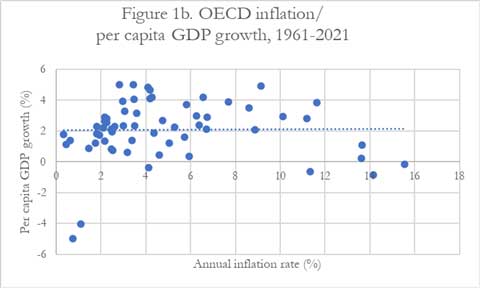

OECD evidence for 1961-2021 – Figures 1a & 1b – updates Bruno & Easterly, again contradicting the ‘standard narrative’ of major CBs, BWIs, BIS and others. The inflation-growth relationship is strongly positive when 1974-75 – severe oil spike recession years – are excluded.

The relationship does not become negative even when 1974-75 are included. Also, the “Great Inflation” of 1965-82 did not harm growth. Hence, there is no empirical basis for setting a particular threshold, such as the now standard 2% inflation target – long acknowledged as “plucked from the air”!

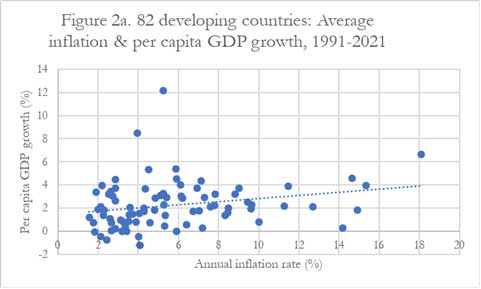

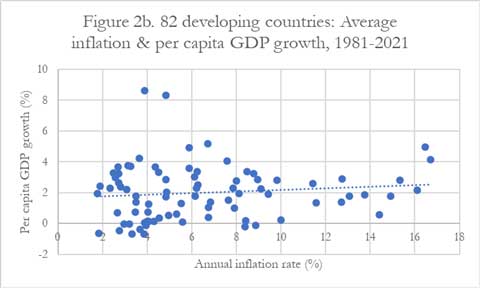

Developing countries also have a positive inflation-growth relationship if extreme cases – e.g., inflation rates in excess of 20%, or ‘excessively’ impacted by commodity price volatilities, civil strife, war – are omitted (Figures 2a & 2b).

Figure 2a summarizes evidence for 82 developing countries during 1991-2021. Although slightly weakened, the positive relationship remained, even if the 1981-90 debt crises years are included (Figure 2b).

Myth 2: Inflation always accelerates

Another popular myth is that once inflation begins, it has an inherent tendency to accelerate. As inflation supposedly tends to speed up, not acting decisively to nip it in the bud is deemed dangerous. So, the IMF chief economist advises, “Don’t let inflation ‘genie’ out of the bottle”. Hence, inflation has to be ‘nipped in the bud’.

But, in fact, OECD inflation has never exceeded 16% in the past six decades, including the 1970s’ oil shock years. Inflation does not accelerate easily, even when labour has more bargaining power, or wages are indexed to consumer prices – as in some countries.

Bruno & Easterly only found a high likelihood of inflation accelerating when inflation exceeded 40%. Two MIT economists – Rüdiger Dornbusch and Stanley Fischer, later International Monetary Fund Deputy Managing Director – came to a similar conclusion, describing 15–30% inflation as “moderate”.

Dornbusch & Fischer also stressed, “Most episodes of moderate inflation were triggered by commodity price shocks and were brief; very few ended in higher inflation”. Importantly, they warned, “such inflations can be reduced only at a substantial … cost to growth”.

Myth 3: Hyperinflation threatens

Although extremely rare, avoiding hyperinflation has become the pretext for central bankers prioritizing inflation prevention. Hyperinflation – at rates over 50% for at least a month – is undoubtedly harmful for growth. But as IMF research shows, “Since 1947, hyperinflations in market economies have been rare”.

Many of the worst hyperinflation episodes in history were after World War Two and the Soviet demise. Bruno & Easterly also mention breakdowns of economic and political systems – as in Iran or Nicaragua, following revolutions overthrowing corrupt despotic regimes.

A White House staff blog noted, “The inflationary period after World War II is likely a better comparison for the current economic situation than the 1970s and suggests that inflation could quickly decline once supply chains are fully online and pent-up demand levels off”.

Myth 4: Evidence-based policymaking

Central bankers love to claim their policymaking is evidence-based. They cite one another and famous economists to enhance the aura of CB “credibility”.

Greater central bank independence (from the executive) has enhanced the influence and power of financial interests – largely at the expense of the real economy. Output and employment growth weakened as a result, worsening the lot of the many, especially in the global South.

Fact: Central banks induce recessions

Inappropriate CB policies have often slowed economic growth without mitigating inflation. Hawkish CB responses to inflation can become self-fulfilling prophecies with high inflation seemingly associated with recessions or growth collapses.

Thus, central bank interventions have caused contractions without reducing inflation. The longest US recession after the Great Depression – in the early 1980s – was due to Fed chair Paul Volcker’s 1979-81 interest rate hikes.

Fearing an “extremely severe” world recession, Columbia University history professor Adam Tooze has summed up the current CBs’ interest rate hike frenzy as “the single most dramatic simultaneous tightening of monetary policy ever”!

Phobias, especially if based on unfounded beliefs, never offer good bases for sound policymaking.

Opinion by Jomo Kwame Sundaram, Anis Chowdhury (sydney and kuala lumpur)

Inter Press Service

SYDNEY and KUALA LUMPUR, Oct 04 (IPS) – Central banks (CBs) around the world – led by the US Fed, European Central Bank and Bank of England – are raising interest rates, ostensibly to check inflation. The ensuing race to the bottom is hastening world economic recession.

Going for broke

New UK Prime Minister Liz Truss has already revived ‘supply side economics’, long thought to have been fatally discredited. Her huge tax cuts are supposed to kick-start Britain’s stagnant economy in time for the next general election.

Anis Chowdhury

But studies of past tax cuts have not found any positive link between lower taxes and economic or employment growth. Oft-cited US examples of Reagan, Bush or Trump tax cuts have been shown to be little more than economic sophistry.

Reagan’s Council of Economic Advisers chairman, Harvard professor Martin Feldstein found most Reagan era growth due to expansionary monetary policy. Volcker’s interest rate hikes to fight inflation were reversed. This enabled the US economy to bounce back from its severe 1982 monetary policy inflicted recession.

After Boris Johnson stepped down, UK Conservative Party leadership contenders started by promising more tax cuts. But The Economist was “sceptical that such cuts will lift Britain’s growth rate”. Instead, it worried tax cuts would compound inflationary pressures, triggering ever tighter monetary policy.

The Economist concluded, “It is hard to spot a connection between the overall level of taxation and long-term prosperity”. Unsurprisingly, The Economist sees Truss’ “largest tax cuts in half a century” as “a reckless budget, fiscally and politically”.

Jomo Kwame Sundaram

While such tax cuts mainly benefit the very rich, the costs of such monetary and fiscal policies are borne by workers and other consumers. Workers are harshly punished by austerity measures, losing both jobs and incomes to interest rate hikes.

Tax cuts usually make things worse. Typically, these require cutting social protection and essential public services, ostensibly to balance the budget. So, already greater wealth and income inequalities will worsen.

Governments have to cut public investments due to ballooning budget deficits. Higher interest rates and public spending cuts will also derail efforts needed to transition to more sustainable, greener futures.

Class war

Policy fights over inflation have many dimensions, including class. Instead of helping people cope with rising living costs, increasing interest rates only makes things worse, hastening economic slowdowns. Thus, workers not only lose jobs and incomes, but also are forced to pay more for mortgages and other debts.

Unemployment, lower incomes, deteriorating health and other pains hurt workers. As workers want higher incomes to cope with rising living expenses, such austere policies are deemed necessary to prevent ‘wage-price spirals’.

As usual, workers are being blamed for the resurgence of inflation. But research by the International Monetary Fund (IMF) and others has found no evidence of such wage-price spirals in recent decades.

Experience and evidence suggest very low likelihood of such dialectics in current circumstances, although some nominal wages have risen. Since the 1980s, labour bargaining power and collective wage determination have declined.

Policymakers should address stagnant, even declining real wages in most economies in recent decades. These have hurt “low-paid workers much more than those at the top”. Even the Organization for Economic Cooperation and Development club of rich countries has “worryingly” noted these trends.

The IMF Deputy Managing Director has explained why wages do not have to be suppressed to avoid inflation. Letting nominal wages rise will mitigate rising inequality, plus declining labour income shares (Figure 1) and real wages.

Source: IMF, World Economic Outlook, April 2017

Profit margins had already risen, even before the Ukraine war and sanctions. US trends prompted the Bloomberg headline, “Fattest Profits Since 1950 Debunk Wage-Inflation Story of CEOs”. Aggregate profits of the largest UK non-financial companies in 2021 rose 34% over pre-pandemic levels.

Policymakers should therefore restrain profits, not wages. Recent price increases have been due to rising profits from mark-ups. Recent trends have made it “easier for firms to put their prices up” notes the Reserve Bank of Australia Governor.

Addressing inequality

The IMF Managing Director (MD) recently warned, “People will be on the streets if we don’t fight inflation”. But people are even more likely to protest if they lose jobs and incomes. Worse, the burden of fighting inflation has been put on them while the elite continues to enrich itself.

Raising interest rates is a blunt means to fight inflation. It worsens living costs and job losses, while tax cuts mainly benefit the rich. Instead, the rich should be taxed more to enhance revenue to increase public provisioning of essential services, such as transport, health and education.

The IMF MD noted raising taxes on the wealthy will help close the yawning gap between rich and poor without harming growth. Public provision of childcare and labour market programmes (e.g., retraining) will improve labour supply. Easing worker shortages can thus dampen price pressures.

The current situation requires addressing growing inequality. Redistributive fiscal measures – taxing high earners to fund expanded social protection and public provisioning – are time-tested means to address disparities.

Increasing top tax rates and tax system progressivity are also socially progressive, checking growing inequality. Meanwhile, as consumer prices spiral, rising profits and high executive remuneration have to be checked.

Supply-side policies

The World Bank and Bank of International Settlements heads have urged reducing the current focus on demand management to counter inflation. They both insist on addressing long-term supply bottlenecks, but do not offer much practical guidance.

Addressing supply bottlenecks can involve tax incentives and credit policies. But discredited supply-side mantras – e.g., labour market deregulation – must be discarded. Related fiscal and monetary policies – e.g., tax cuts for the rich and inappropriate interest rate hikes – should also be abandoned.

Governments are losing chances to boost productivity, achieve low carbon transformation and cut inequalities. Instead, policymakers should pro-actively push desired economic changes by favouring less carbon-intensive and more dynamic investments.

Governments must rise to the extraordinary challenges of our times with pragmatic, appropriate and progressive policy initiatives. To do this well, they must boldly reject the ideologies and dogmas responsible for our current predicament.

Opinion by Jomo Kwame Sundaram, Anis Chowdhury (sydney and kuala lumpur)

Inter Press Service

SYDNEY and KUALA LUMPUR, Sep 27 (IPS) – Inflation phobia among central banks (CBs) is dragging economies into recession and debt crises. Their dogmatic beliefs prevent them from doing right. Instead, they take their cues from Washington: the US Fed, Treasury and Bretton Woods institutions (BWIs).

Costly recessions

Both BWIs – the International Monetary Fund (IMF) and World Bank – have recently raised the alarm about the likely dire consequences of the ensuing contractionary ‘race to the bottom’. But their dogmas stop them from being pragmatic. Hence, their policy analyses and advice come across as incoherent, even contradictory.

Anis Chowdhury

Ominously, the Bank has warned, “he global economy is now in its steepest slowdown following a post-recession recovery since 1970”. As “central banks across the world simultaneously hike interest rates in response to inflation, the world may be edging toward a global recession in 2023”.

Warning “Increased interest rates will bite”, the IMF Managing Director has urged countries to “buckle up”, acknowledging anti-inflationary measures threaten recovery. “For hundreds of millions of people it will feel like a recession, even if the world economy avoids” two consecutive quarters of contracting output.

She also noted US Fed rate hikes have strengthened the dollar, raising import costs and making it costlier to service dollar-denominated debt. But reciting the mantra, she claims if inflation “gets under control, then we can see a foundation for growth and recovery”.

This contradicts all evidence that low inflation comes at the expense of robust growth. Per capita output growth and productivity growth both fell during three decades of low inflation. Also, low inflation has not prevented financial crises.

Even if growth recovers, recessions’ scars remain. For example, an IMF study found, “the Great Recession of 2007–09 has left gaping wounds”. Over 200 million people are unemployed worldwide, over 30 million more than in 2007.

A 2018 San Francisco Fed study assessed the Great Recession cost Americans about $70,000 each. The Harvard Business Review estimated, over 2008-10, it cost the US government “well over $2 trillion, more than twice the cost of the 17-year-long war in Afghanistan”.

Jomo Kwame Sundaram

Counting the costs

“The human and social costs are more far-reaching than the immediate temporary loss of income.” Such effects are typically much greater for the most vulnerable, e.g., the youth and long-term unemployed.

Studies have documented its harmful impacts on wellbeing, particularly mental health. Recessions in Europe and North America caused over 10,000 more suicides, greater drug abuse and other self-harming behaviour. Adverse socio-economic and health impacts are worse in developing countries with poor social protection.

Interest rate hikes during 1979-82 triggered debt crises in over 40 developing countries. The 1982 world recession “coincided with the second-lowest growth rate in developing economies over the past five decades, second only to 2020”. A “decade of lost growth in many developing economies” followed.

But Bank research shows interest rate hikes “may not be sufficient to bring global inflation back down”. The Bank even warns major CBs’ anti-inflationary measures may trigger “a string of financial crises in emerging market and developing economies”, which “would do them lasting harm”.

Developing country governments’ external debt – increasingly commercial, costing more and repayable sooner – has ballooned since the 2008-09 global financial crisis. The pandemic has caused more debt to become unsustainable as rich countries oppose meaningful relief.

No policy consensus

The Bank correctly notes, “A slowdown … typically calls for countercyclical policy to support activity”. It acknowledges, “the threat of inflation and limited fiscal space are spurring policymakers in many countries to withdraw policy support even as the global economy slows sharply”.

It also suggests, “policymakers could shift their focus from reducing consumption to boosting production…to generate additional investment and improve productivity and capital allocation…critical for growth and poverty reduction.”

However, it does not offer much policy guidance besides the usual irrelevant platitudes, e.g., CBs “must communicate policy decisions clearly while safeguarding their independence”.

It even blames “labor-market constraints”. For decades, the Bank promoted measures to promote labour market flexibility, ostensibly to increase participation rates, reduce prices, via wages, and re-employ displaced workers.

Such policies since the 1980s have accelerated declining productivity growth and real incomes for most. They have reduced labour’s share of national income, increasing inequality. To make matters worse, the Bank misleadingly attributes many policy-induced economic woes to high inflation.

In May, the IMF Deputy Managing Director argued wages did not have to be suppressed to avoid inflation. She called for CB vigilance and “forceful” actions against inflation, which “will remain significantly above central bank targets for a while”.

No more Washington Consensus

In June, a Fund policy note advised allowing “a full pass-through of higher international fuel prices to domestic users”. It advised recognizing the supply shock causes of contemporary inflation and protecting the most vulnerable.

But more alarmist Fund staff urge otherwise. In July, its ‘chief economist’ urged, “bringing back to central bank targets should be the top priority … Central banks that have started tightening should stay the course until inflation is tamed”.

Although he acknowledged, “ighter monetary policy will inevitably have real economic costs”, without any evidence, he insisted, “delaying it will only exacerbate the hardship”.

In August, the Bank of International Settlements (BIS) head urged shifting attention from managing demand to enabling supply. He warned central bankers had for too long assumed that supply adjusts automatically and smoothly to shifts in demand.

He warned, “Continuing to rely primarily on aggregate demand tools to boost growth in this environment could increase the danger, as higher and harder-to-control inflation could result”.

But the BIS ‘chief economist’ soon urged major economies to “forge ahead with forceful” interest rate hikes despite growing threats of recession. He did not seem to care that the rate hike gamble to fight inflation may not work and its costs could be astronomical.

Inflation fear mongering

Influential economists at the US Fed, Bank of England, Fund and BIS fear “second-round” effects of mainly supply-shock inflation due to “wage-price spirals”.

But Fund research acknowledged, “little empirical research …… the effects of oil price shocks on wages and factors affecting their strength”. It found very low likelihood of such ‘pass-through’ effects due to significant labour market changes, including drastic declines in unionization and collective bargaining.

It reported “almost zero pass-through for 1980-1999” and negligible effects during 2000-19, before concluding, “In a broad stroke, the pass-through has declined over time in Europe”. Similar findings have been reported by others.

Reserve Bank of Australia (RBA) research found “the current episode has many differences to the 1970s, when a wage-price spiral did emerge”. It concluded, “There are a number of factors that work against a wage-price spiral emerging, … implying that the overall risk in most advanced economies is probably quite low”.

Australian professor Ross Garnaut has suggested, “the spectre of a virulent wage-price spiral comes from our memories and not current conditions”. Sadly, despite all the evidence, including their own, the Fund and RBA still urge firm CB actions against inflation!

Opinion by Jomo Kwame Sundaram, Anis Chowdhury (sydney and kuala lumpur)

Inter Press Service

SYDNEY and KUALA LUMPUR, Sep 20 (IPS) – Policymakers have become obsessed with achieving low inflation. Many central banks adopt inflation targeting (IT) monetary policy (MP) frameworks in various ways. Some have mandates to keep inflation at 2% over the medium term. Many believe this ensures sustained long-term prosperity.

Anis ChowdhuryThe now universal 2% inflation target “was plucked out of the air”. This was acknowledged by Reserve Bank of New Zealand (RBNZ) Governor Don Brash who first adopted IT. The target was due to NZ Finance Minister Roger Douglas’ “chance remark” of achieving “genuine price stability, around 0, or 0 to 1 percent”.

IT discord

Heads of major central banks – such as the US Federal Reserve Bank (Fed), Bank of England (BoE) and German Bundesbank – committed to keep inflation at 2% soon after NZ. Although typically ‘medium-term’, IT’s high costs are portrayed as necessary, but brief. Worse, promised growth benefits have not materialized.

The Articles of Agreement of the International Monetary Fund (IMF) never endorsed any fixed inflation target. Article IV states, “each member shall: (i) endeavor to direct its economic and financial policies toward the objective of fostering orderly economic growth with reasonable price stability, with due regard to its circumstances”.

This makes clear much depends on conditions and circumstances. The sensible priority then would be to sustain prosperity with “reasonable price stability”, and not to commit to an arbitrary universal IT at any cost. Yet, many IMF officials promote the 2% target.

Jomo Kwame SundaramDuring the 2008-09 global financial crisis (GFC), the IMF Managing Director appealed for more imagination in designing monetary policy, appreciating “just how intricate the global economic and financial web had become”.

For him, “Monetary policy needs to look beyond its core focus on low and stable inflation” to promote balanced and equitable growth, while minimizing adverse spill-overs on developing economies.

A Bank of Canada working paper concluded, “the current state of economic research – both empirical and theoretical – provides little basis for believing in significant observable benefits of low inflation such as an increase in the growth rate of real GDP”.

IT benefits?

Any objective consideration of actual IT experiences would have led to its rejection long ago. IT is clearly inimical to growth and equity, let alone the Sustainable Development Goals (SDGs). Four central bank (CB) experiences offer valuable lessons about IT’s likely consequences.

The US Fed is, by far, the most important CB globally, while the BoE has been historically important. The Bundesbank has been the most inflation averse in the post-war period, while the RBNZ was the world’s IT pioneer.

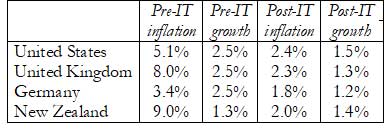

NZ’s inflation during 1961-90 averaged 9%, more than the US’s 5.1% and the UK’s 8%. Yet, the mighty Fed and the venerable BoE sought to emulate the miniscule RBNZ! Germany’s well-known inflation-phobia is attributed to its inter-war ‘hyperinflation’ and its bloody aftermath. Inflation there averaged 3.4% over 1960-90, i.e., even before IT.

None achieved sustained economic prosperity despite reaching inflation targets of 2% or less. Average per capita GDP growth declined sharply in the US, UK and Germany, while rising negligibly in NZ (Table 1).

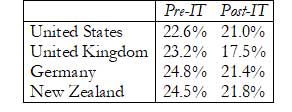

Long-term declines in their growth rates followed declining investments (Table 2). IT advocates claim high inflation causes uncertainty, thus reducing investments, but lower inflation has clearly done worse.

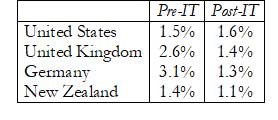

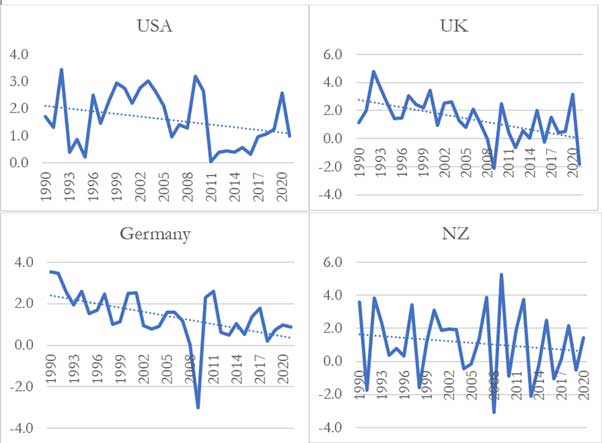

As the investment rate declined with IT, so did productivity growth in the UK, Germany and NZ (Table 3). While productivity growth has risen negligibly with IT in the US, it has trended down in all four economies (Figures 1-4). US hourly output grew at only 1.4% after 2004, “half its pace in the three decades after World War II”.

Most advanced economies have experienced productivity slowdowns since the 1970s. With the European Central Bank’s strict IT framework, the euro zone also saw marked slowdowns in productivity growth during 1999-2019.

Declining productivity growth often becomes the pretext for depressing real wages and working conditions, compelling workers to work more to compensate for lost earnings. Productivity and growth slowdowns are seen as “secular stagnation”.

All this has been blamed on inflation. But lowering inflation has not reversed this trend, which has actually accelerated since the GFC. Many explanations have been offered, but the reasons for this failure remain moot.

IT, low inflation, tax cuts and market reforms are supposed to improve economic performance. Weaker investment and economic growth, due to contractionary macroeconomic policies, slowed US productivity growth.

Similarly, The Economist observed, “Drooping demand crimped incentives to invest and innovate”. It ascribed declining UK productivity growth to cuts in innovation investments due to “austerity policies” and “severe reduction in credit”, inter alia.

Concluding “no doubt … the cost … was huge”, it estimated, “Britain’s GDP per person in 2019 would have been £6,700 ($8,380) higher than it turned out to be” had productivity growth not fallen further after the GFC.

There is growing acknowledgement that widespread “unconditional” CB commitment to 2% inflation targets – in the face of the current inflationary upsurge – is likely to worsen slowdowns. This is likely to compound debt crises in many developing countries.

The adverse socio-economic impacts of recessions are well documented. Policy-induced recessions – supposedly to curb inflation – will compound the effects of pandemic, war and sanctions.

Pragmatism, not dogma

Central bankers should not be dogmatic. Instead, pragmatic approaches are urgently needed to address the current inflationary surges. This is especially necessary when inflation worldwide is mainly due to supply shocks.

Western policymakers must consider the adverse spill-over impacts on developing countries, already on the brink of debt crises due to protracted slowdowns. Government debt – with more higher cost commercial borrowings – has been rising since the GFC, Western ‘quantitative easing’ and Covid-19.

Almost all central bankers know it is almost impossible to achieve 2% inflation in current circumstances. Yet, they insist not raising interest rates now will cause much economic damage later.

But such claims clearly have no theoretical or empirical bases. Hence, it is recklessly dogmatic to enforce a 2% target by falsely claiming inaction would be even more harmful.

Opinion by Jomo Kwame Sundaram, Anis Chowdhury (sydney and kuala lumpur)

Inter Press Service

SYDNEY and KUALA LUMPUR, Sep 06 (IPS) – As rich countries raise interest rates in double-edged efforts to address inflation, developing countries are struggling to cope with slowdowns, inflation, higher interest rates and other costs, plus growing debt distress.

Rich countries’ interest rate hikes have triggered capital outflows, currency depreciations and higher debt servicing costs. Developing country woes have been worsened by commodity price volatility, trade disruptions and less foreign exchange earnings.

Anis ChowdhuryRising debt risks Almost 60% of the poorest countries were already in, or at high risk of debt distress, even before the Ukraine crisis. Debt service burdens in middle-income countries have reached 30-year highs, as interest rates rise with food, fertilizer and fuel prices.

Developing countries’ external debt has risen since the 2008-09 global financial crisis (GFC) – from $2 trillion (tn) in 2000 to $3.4tn in 2007 and $9.6tn in 2019! External debt’s share of GDP fell from 33.1% in 2000 to 22.8% in 2008. But with sluggish growth since the GFC, it rose to 30% in 2019, before the pandemic.

The pandemic pushed up developing countries’ external debt to $10.6tn, or 33% of GDP in 2020, the highest level on record. The external debt/GDP ratio of developing countries other than China was 44% in 2020.

Borrowing from international capital markets accelerated after the GFC as interest rates fell. But commercial debt is generally of shorter duration, typically less than ten years. Private lenders also rarely offer restructuring or refinancing options.

Lenders in international capital markets charge developing countries much higher interest rates, ostensibly for greater risk. But changes in public-private debt composition and associated costs have made such debt riskier.

Meanwhile, unguaranteed private debt now exceeds public debt. Although private debt may not be government-guaranteed, states often have to take them on in case of default. Hence, such debt needs to be seen as potential contingent government liabilities.

Jomo Kwame SundaramSri Lankan international capital market borrowings grew from 2.5% of foreign debt in 2004 to 56.8% in 2019! Its dollar denominated debt share rose from 36% in 2012 to 65% in 2019, while China accounted for 10% of its external borrowings.

Private borrowings for less than ten years were 60% of Lankan debt in April 2021. The average interest rate on commercial loans in January 2022 was 6.6% – more than double the Chinese rate. In 2021, Lankan interest payments alone came to 95.4% of its declining government revenue!

More commercial borrowing

Thus, external debt increasingly involved more speculative risk. Public bond finance, foreign debt’s most volatile component, rose relative to commercial bank loans and other private credit. Meanwhile, more stable and less onerous official credit has declined in significance.

Various factors have made things worse. First, most rich countries have failed to make their promised annual aid disbursements of 0.7% of their gross national income, made more than half a century ago.

Worse, actual disbursements have actually declined from 0.54% in 1961 to 0.33% in recent years. Only five nations have consistently met their 0.7% promise. In the five decades since promising, rich economies have failed to deliver $5.7tn in aid!

Sustainable development outcomes of such private financing – especially in promoting poverty reduction, equity and health – have been mixed at best. But private finance has nonetheless imposed heavy burdens on government budgets.

Third, since the GFC, developed economies have resorted to unconventional monetary policies – ‘quantitative easing’, with very low or even negative real interest rates. With access to cheap funds, managers seeking higher returns invested lucratively in emerging markets before the recent turnaround.

Large investment funds and their collaborators, e.g., credit rating agencies, have profitably created new means to get developing countries to float more bonds to raise funds in international capital markets.

Favouring private market solutions, donors, MDBs and the IMF have discouraged pro-active development initiatives for over four decades. Hence, many developing countries remain primary producers with narrow export bases and volatile earnings.

They have urged debilitating reforms, e.g., arguing tax cuts are necessary to attract foreign direct investment (FDI). Meanwhile, corporate tax evasion and avoidance have worsened developing countries’ revenue losses. Thus, net revenue has fallen as such reforms fail to generate enough growth and revenue.

Credit rating agencies often assess developing countries unfavourably, raising their borrowing costs. Quick to downgrade emerging markets, they make it costlier to get financing, even if economic fundamentals are sound.

The absence of orderly and fair debt restructuring mechanisms has not helped. Commercial lenders charge higher interest rates, ostensibly for default risks. But then, they refuse to refinance, restructure or provide relief, regardless of the cause of default.

When will we learn?

Following the 1970s’ oil price hikes, western, especially US banks were swimming in liquidity as oil exporters’ dollar reserves swelled. These banks pushed debt, getting developing country governments to borrow at low real interest rates.

After the US Fed began raising interest rates from 1977 to fight inflation, other major central banks followed, raising countries’ debt service burdens. Ensuing economic slowdowns cut commodity exporters’ earnings.

In the past, the IMF and World Bank imposed ‘one-size-fits-all’ ‘stabilization’ and ‘structural adjustment’ measures, impairing development. Developing countries had to implement severe austerity measures, liberalization and privatization. As real incomes declined, progress was set back.

With the pandemic, developing countries have seen massive capital outflows, more than in 2008. Meanwhile, surging food, fertilizer and fuel prices are draining developing countries’ foreign exchange earnings and reserves.

As the US Fed raises interest rates, capital flight to Wall Street is depreciating other currencies, raising import costs and debt burdens. Thus, many countries need financial help.

Debt-distressed countries once again seek support from the Washington-based lenders of last resort. But without enough debt relief, a temporary liquidity crisis threatens to become a debt sustainability, and hence, a solvency crisis, as in the 1980s.

A partial view of the city of Punto Fijo, with the Cardón refinery in the background, on the Paraguaná peninsula, projected as a special economic zone overlooking the Caribbean in northwest Venezuela. CREDIT: Megaconstrucciones

by Humberto Marquez (caracas)

Inter Press Service

CARACAS, Sep 03 (IPS) – Venezuela is preparing to replicate the experience of Special Economic Zones (SEZs), a mechanism with which more than 60 countries have tried to draw investment and accelerate economic growth, while under its avowedly socialist government a “silent neoliberalism” is gaining ground.

The aim of the SEZs is “to provide special conditions to gain the economic confidence of investors from all over the world, and productive development to put an end once and for all to oil rentism,” said President Nicolás Maduro when he promulgated the Organic Law of Special Economic Zones on Jul. 20.

The SEZs, “90 percent of which are in the global developing South, are a catalyst for economic restructuring processes and go hand in hand with the expansion of the neoliberal economy,” sociologist Emiliano Terán, a researcher with the non-governmental Venezuelan Observatory of Political Ecology, told IPS.

According to the United Nations Conference on Trade and Development (Unctad), there were 5,383 SEZs in the world in 2019 and another 508 under construction, of which 4,772 were in developing countries – 2,543 in China alone and 737 in Southeast Asia.

In Latin America and the Caribbean there were 486 – 73 in the Dominican Republic, some 150 in Central America, seven in Mexico and 39 in Colombia.

SEZs are mainly commercial, such as free ports or free trade zones, where import quotas, tariffs, customs or sales taxes are eliminated; industrial, with an emphasis on improving infrastructure available to companies; urban or mining ventures; or export processing.

Their main characteristic is that, in order to stimulate investment, especially foreign investment, there are more flexible regulations on taxes, investment requirements, employment, paperwork and procedures, access to resources and inputs, export quotas and capital repatriation.

One of the camping areas improvised by tour operators on La Tortuga, an island with no permanent population where tourist developments are being planned that are triggering environmentalist alarms, as they may severely affect the still almost pristine ecosystem of the island and its surrounding Caribbean waters. CREDIT: Jorge Muñoz/Aleteia

An eye on the environment

In Venezuela, the first five zones decreed are the arid Paraguaná Peninsula, in the northwest; Margarita Island, in the southeastern Caribbean; La Guaira and Puerto Cabello, which are the largest ports, along the central portion of the Caribbean coast; and the remote La Tortuga Island, some 200 kilometers northeast of Caracas.

Paraguaná (an area of 3,400 square kilometers) is home to a large oil refining complex, and Margarita Island (1,020 square kilometers) has for decades been a sales tax-free zone and a tourist mecca for Venezuela’s middle class.

Puerto Cabello and La Guaira are essentially ports for imports to the populated north-central part of the country, whose main exports, oil and metals, are shipped from docks in the production areas in the east and west.

Hotel complexes, airports, marinas and golf courses are being planned for La Tortuga, which covers 156 square kilometers and has no permanent population. Environmental groups warn that its waters, reefs and the island itself are home to five species of turtles, 73 species of birds and dozens of species of fish and cetaceans.

Sociologist Emiliano Terán (R) with economists Luis Crespo (C) and Carlos Lazo (L) take part in a forum at the Central University of Venezuela critical of the announced special economic zones. CREDIT: Humberto Márquez/IPS

Limited economy

“The environmental issue is a concern, but it is hard to believe that the government has the resources or the investors for the number of hotels planned for La Tortuga,” economist Luis Oliveros, a professor at the Metropolitan and Central Universities of Venezuela, told IPS.

The decreed Venezuelan SEZs “seem more like announcements than realities, and although we like the government to think of growth and development hand in hand with private investment, much more is needed. It has yet to be clarified what exactly the government is pursuing with these zones,” Oliveros said.

In Venezuela “creating SEZs has limitations, such as the sanctions (imposed by the United States and the European Union) and the need to generate macroeconomic stability and legal certainty, which are pending issues,” he added.

After seven years of sharp decline – and three years of hyperinflation – Venezuela’s annual gross domestic product, which exceeded 300 billion dollars a decade ago, now stands between 50 and 60 billion dollars, according to economists.

Oil production, the main lever of the economy and source of tax revenues, has shrunk and is starved of new investments, while the State desperately seeks income by exporting crude oil at a discount or selling gold that is extracted at the cost of great environmental damage in the southeast of the country.

Attracting investment may be an uphill struggle for SEZs that have still not been fully mapped out, considering that, for example, major companies have not knocked on the door to raise oil production – 600,000 barrels per day when a decade ago it was three million – despite the favorable signals sent by the United States.

Since March, informal contacts between Washington and Caracas, prompted by the impact of the war in Ukraine on the world energy market, have explored, without success so far, easing sanctions and other measures to bring Venezuela back to the U.S. oil market with new investments.

Juan Griego Bay in the north of Margarita Island, already half a century old as a sales tax-free zone and tourist mecca for Venezuela’s middle class, is now one of the country’s five special economic zones. CREDIT: Mipci

Neoliberal plan

In the southeast of the country, an area rich in gold, iron, diamonds, coltan and other minerals, the 112,000 square kilometer Orinoco Mining Arc (larger than Bulgaria, Cuba or Portugal) was decreed in 2016 as a “strategic development zone”, and its control and management was handed over to the armed forces.

The Mining Arc “has been a precedent for a new model promoted by the State to attract investments, but with depredation of the environment and restriction of wages and workers’ rights,” warned Luis Crespo, professor of Economics at the Central University of Venezuela, during a forum at that university.

“The special economic zones are part of a silent neoliberal adjustment plan driven forward by the government of President Maduro,” said Crespo.

The Venezuelan SEZ law – enacted by the legislature, which has been boycotted by most of the political opposition – states that its purpose is to develop a new production model, promote domestic and foreign economic activity, and diversify and increase exports.

It also aims to promote innovation, industry and technology transfer, create jobs and “ensure the environmental sustainability of production processes.”

The terminology about socialism or transition to socialism, frequent in the political discourse of the government and the ruling United Socialist Party, is absent from the legislation of the SEZs and from the repeated calls for private capital.

“The example of China is being followed, as it is by other countries, in using the SEZs as a showcase for heterodox forms of capital accumulation, in a process of progressive neoliberalization of the economy, as the oil model of production and distribution of wealth is being exhausted,” Terán said.

He added that “the SEZs cannot be seen only in terms of macroeconomic indicators,” as they become “zones of social and environmental sacrifice, with a new political geography of dispossession, and with the cheapening of labor, especially that of women workers.”

According to UNCTAD, although there are differences in SEZs from one country to another and within countries, their common features include having a clearly defined geographic area, a regulatory regime that is distinct from the rest of the economy, and special infrastructure support for the development of their activities.

A view of the border crossing between Colombia and Venezuela over the Simón Bolívar Bridge (in southwest Venezuela and northeast Colombia), when there was free transit and intense activity before the border was closed and relations between the two countries broke down. Now Caracas proposes to create a binational special economic zone in the area. CREDIT: Humberto Márquez/IPS

More politics

Venezuela’s SEZs will be guided by a council to be freely appointed by the president, each will have a single authority to be named by the president, and the decree establishing one of the zones must be considered by the legislature within 10 working days or it will be approved, without discussion.

Areas such as the SEZs, the Mining Arc or special military zones in practice modify the political-administrative division of the country, which only in theory is a federal republic with 23 states plus a capital district.

In another political move, on Aug. 23 Maduro publicly proposed to his new Colombian counterpart, leftwing President Gustavo Petro, who took office on Aug. 7, the creation of a special binational economic zone between southwestern Venezuela and northeastern Colombia.

“We are going to propose to President Petro the construction of a large economic, commercial and productive zone between the department of Norte de Santander (Colombia) and the state of Táchira (Venezuela),” Maduro said.

Diplomatic, political, commercial and transit relations between the neighboring countries have been severed since February 2019.

In Táchira, business spokespersons have expressed their support for this Andean state of 11,000 square kilometers to obtain special regimes that favor trade with the neighboring country, and their peers in Colombia are betting on a recovery of bilateral trade, which prospered until the first decade of this century.

Terán described the projected creation of the SEZs as a possible “new pact of elites in Venezuela,” after more than 20 years of acute political confrontation, but warned that “there is an alternative, because although fragmented, dispersed and with a new look, protests against these pacts have never ceased.”

Opinion by Jomo Kwame Sundaram, Anis Chowdhury (sydney and kuala lumpur)

Inter Press Service

SYDNEY and KUALA LUMPUR, Aug 30 (IPS) – Most sub-Saharan African French colonies got formal independence in the 1960s. But their economies have progressed little, leaving most people in poverty, and generally worse off than in other post-colonial African economies.

Decolonization?

Pre-Second World War colonial monetary arrangements were consolidated into the Colonies Françaises d’Afrique (CFA) franc zone set up on 26 December 1945. Decolonization became inevitable after France’s defeat at Dien Bien Phu in 1954 and withdrawal from Algeria less than a decade later.

CFA countries are now in two currency unions. Benin, Burkina Faso, Côte d’Ivoire, Guinea-Bissau, Mali, Niger, Senegal and Togo belong to UEMOA, the French acronym for the West African Economic and Monetary Union.

Its counterpart CEMAC is the Economic and Monetary Community of Central Africa, comprising Cameroon, the Central African Republic, the Republic of the Congo, Gabon, Equatorial Guinea and Chad.

Both UEMOA and CEMAC use the CFA franc (FCFA). Ex-Spanish colony, Equatorial Guinea, joined in 1985, one of two non-French colonies. In 1997, former Portuguese colony, Guinea-Bissau was the last to join.

Such requirements have ensured France’s continued exploitation. Eleven of the 14 former French West and Central African colonies remain least developed countries (LDCs), at the bottom of UNDP’s Human Development Index (HDI).

Guinea soon faced French destabilization efforts. Counterfeit banknotes were printed and circulated for use in Guinea – with predictable consequences. This massive fraud brought down the Guinean economy.

Jomo Kwame Sundaram

France withdrew more than 4,000 civil servants, judges, teachers, doctors and technicians, telling them to sabotage everything left behind: “un divorce sans pension alimentaire” – a divorce without alimony.

Togo independence leader, President Sylvanus Olympio was assassinated in front of the US embassy on 13 January 1963. This happened a month after he established a central bank, issuing the Togolese franc as legal tender. Of course, Togo remained in the CFA.

Mali left the CFA in 1962, replacing the FCFA with the Malian franc. But a 1968 coup removed its first president, radical independence leader Modibo Keita. Unsurprisingly, Mali later re-joined the CFA in 1984.

Resource-rich

The eight UEMOA economies are all oil importers, exporting agricultural commodities, such as cotton and cocoa, besides gold. By contrast, the six CEMAC economies, except the Central African Republic, rely heavily on oil exports.

CFA apologists claim pegging the FCFA to the French franc, and later, the euro, has kept inflation low. But lower inflation has also meant “slower per capita growth and diminished poverty reduction” than in other African countries.

The CFA has “traded decreased inflation for fiscal restraint and limited macroeconomic options”. Unsurprisingly, CFA members’ growth rates have been lower, on average, than in non-CFA countries.

Its oil boom ensured growth averaging 23.4% annually during 2000–08. But growth has fallen sharply since, contracting by -5% yearly during 2013–21! Its 2019 HDI of 0.592 ranked 145 of 189 countries, below the 0.631 mean for middle-ranking countries.

Four of ten 6–12 year old children in Equatorial Guinea were not in school in 2012, many more than in much poorer African countries. Half the children starting primary school did not finish, while less than a quarter went on to middle school.

CFA member Gabon, the fifth largest African oil producer, is an upper middle-income country. With petroleum making up 80% of exports, 45% of GDP, and 60% of fiscal revenue, Gabon is very vulnerable to oil price volatility.

One in three Gabonese lived in poverty, while one in ten were in extreme poverty in 2017. More than half its rural residents were poor, with poverty three times more there than in urban areas.

Côte d’Ivoire, a non-LDC CFA member, enjoyed high growth, peaking at 10.8% in 2013. With lower cocoa prices and Covid-19, growth fell to 2% in 2020. About 46% of Ivorians lived on less than 750 FCFA (about $1.30) daily, with its HDI ranked 162 of 189 in 2019.

Credit-GDP ratios in CFA countries have been low at 10–25% – against over 60% in other Sub-Saharan African countries! Low credit-GDP ratios also suggest poor finance and banking facilities, not effectively funding investments.

By surrendering exchange rate and monetary policy, CFA members have less policy flexibility and space for development initiatives. They also cannot cope well with commodity price and other challenges.

The CFA’s institutional requirements – especially keeping 70% of their foreign exchange with the French Treasury – limit members’ ability to use their forex earnings for development.

More recent fiscal rules limiting government deficits and debt – for UEMOA from 2000 and CEMAC in 2002 – have also constrained policy space, particularly for public investment.

Unrestricted transfers to France have enabled capital flight. The FCFA’s unlimited euro convertibility is supposed to reduce foreign investment risk in the CFA. However, foreign investment is lower than in other developing countries.

Controlling the loss and waste of food is a crucial factor in reaching the goal of eradicating hunger in the world. Credit: FAO

by Thalif Deen (united nations)

Inter Press Service

UNITED NATIONS, Aug 22 (IPS) – The ominous warnings keep coming non-stop: some of the world’s developing nations, mostly in Africa and Asia, are heading towards mass hunger and starvation.

The World Food Programme (WFP) warned last week that as many as 828 million people go to bed hungry every night while the number of those facing acute food insecurity has soared — from 135 million to 345 million — since 2019. A total of 50 million people in 45 countries are teetering on the edge of famine.

But in what seems like a cruel paradox the US Department of Agriculture estimates that a staggering $161 billion worth of food is dumped yearly into landfills in the United States.

The shortfall has been aggravated by reduced supplies of wheat and grain from Ukraine and Russia triggered by the ongoing conflict, plus the after-effects of the climate crisis, and the negative spillover from the three-year long Covid-19 pandemic.

While needs are sky-high, resources have hit rock bottom. The WFP says it requires $22.2 billion to reach 152 million people in 2022. However, with the global economy reeling from the COVID-19 pandemic, the gap between needs and funding is bigger than ever before.

Controlling the loss and waste of food is a crucial factor in reaching the goal of eradicating hunger in the world. Credit: FAO

“We are at a critical crossroads. To avert the hunger catastrophe the world is facing, everyone must step up alongside government donors, whose generous donations constitute the bulk of WFP’s funding. Private sector companies can support our work through technical assistance and knowledge transfers, as well as financial contributions. High net-worth individuals and ordinary citizens alike can all play a part, and youth, influencers and celebrities can raise their voices against the injustice of global hunger,” the Rome-based agency said.

In 2019, Russia and Ukraine together exported more than a quarter (25.4 percent) of the world’s wheat, according to the Observatory of Economic Complexity (OEC).

Danielle Nierenberg, President and Founder, Food Tank told IPS the amount of food that is wasted the world is not only a huge environmental problem–if food waste were a country, it would be the third largest emitter of greenhouse gas emissions.

But food waste and food loss are also moral conundrums. It’s absurd to me that so much food is wasted or lost because of lack of infrastructure, poor policymaking, or marketing regulations that require food be thrown away if it doesn’t fit certain standards.

This is especially terrible now as we face a worldwide food crisis–not only because of the Russian aggression against Ukraine, but multiple conflicts all over the globe.

“We’ve done a good job over the last decade of creating awareness around food waste, but we haven’t done enough to actually convince policymakers to take concrete action. Now is the time for the world to address the food waste problem, especially because we know the solutions and many of them are inexpensive,” she said.

Better regulation around expiration and best buy dates, policies that separate organic matter in municipalities, fining companies that waste too much, better date collection around food waste, more infrastructure and practical innovations that help farmers.

“And there are even more solutions. We can solve this problem–and we have the knowledge. We just need to implement it,” said Nierenberg.

The US Food and Drug Administration (FDA) said last November food waste in the United States is estimated at between 30–40 percent of the food supply.

“Wasted food is the single largest category of material placed in municipal landfills and represents nourishment that could have helped feed families in need. Additionally, water, energy, and labor used to produce wasted food could have been employed for other purposes’, said the FDA.

Effectively reducing food waste will require cooperation among federal, state, tribal and local governments, faith-based institutions, environmental organizations, communities, and the entire supply chain.

Professor Dr David McCoy, Research Lead at United Nations University International Institute for Global Health (UNU-IIGH), told IPS the heartbreaking image of food being dumped in landfills while famine and food insecurity grows, must also be juxtaposed with the ecological harms caused by the dominant modes of food production which in turn will only further deepen the crisis of widespread food insecurity.

“The need for radical and wholesale transformation to the way we produce, distribute and consume food has been recognized for years. However, powerful actors – most notably private financial institutions and the giant oligopolist corporations who make vast profits from the agriculture and food sectors – have a vested interest in maintaining the status quo. Their resistance to change must be overcome if we are to avoid a further worsening of the hunger and ecological crises, he warned”.

Frederic Mousseau, Policy Director at the Oakland Institute, told IPS that according to the Food and Agriculture Organization (FAO), global food production and stocks are at historic high levels in 2022, with only a slight contraction compared to 2021.

“Skyrocketing food prices seen this year are rather due to speculation and profiteering than the war in Ukraine. It is outrageous that WFP has been forced to expand its food relief operations around the world due to speculation, while also having to raise more funds as the costs of providing food relief has increased everywhere”, he said.

Mousseau pointed out that WFP’s costs increased by $136 million in West Africa alone due to high food and fuel prices, whereas at the same time, the largest food corporations announced record profits totaling billions.

Louis Dreyfus and Bunge Ltd had respectively 82.5% and 15% jump in profits so far this year. Cargill had a 23% jump in its revenue. Profits of a handful of food corporations that dominate the global markets already exceed $10 billion this year – the equivalent of half of the $22 billion that WFP is seeking to address the food needs of 345 million people in 82 countries.

At a press conference in Istanbul, UN Secretary-General Antonio Guterres held out a glimmer of hope when he told reporters August 20 that more than 650,000 metric tons of grain and other food are already on their way to markets around the world.

“I just came back from the Marmara Sea, where Ukrainian, Russian, Turkish and United Nations teams, are conducting joint inspections on the vessels passing through the Black Sea on their way in or out of the Ukrainian ports. What a remarkable and inspiring operation.”

“I just saw a World Food Progamme-chartered vessel – Brave Commander – which is waiting to sail to the horn of Africa to bring urgently needed relief to those suffering from acute hunger. Just yesterday, I was in Odesa port and saw first-hand the loading on a cargo of wheat onto a ship.

He said he was “so moved watching the wheat fill up the hold of the ship. It was the loading of hope for so many around the world.”

“But let’s not forget that what we see here in Istanbul and in Odesa is only the more visible part of the solution. The other part of this package deal is the unimpeded access to the global markets of Russian food and fertilizer, which are not subject to sanctions.”

Guterres pointed out that it is important that all governments and the private sector cooperate to bring them to market. Without fertilizer in 2022, he said, there may not be enough food in 2023.

Getting more food and fertilizer out of Ukraine and Russia is critical to further calm commodity markets and lower prices for consumers

“We are at the beginning of a much longer process, but you have already shown the potential of this critical agreement for the world.

And so, I am here with a message of congratulations for all those in the Joint Coordination Centre and a plea for that vital life-saving work to continue.

You can count on the full commitment of the United Nations to support you,” he declared.

Opinion by Jomo Kwame Sundaram, Anis Chowdhury (sydney and kuala lumpur)

Inter Press Service

SYDNEY and KUALA LUMPUR, Aug 16 (IPS) – Half a century after the 1970s’ stagflation, economies are slowing, even contracting, as prices rise again. Thus, the World Bank warns, “Surging energy and food prices heighten the risk of a prolonged period of global stagflation reminiscent of the 1970s.”

In March, Reuters reported, “With surging oil prices, concerns about the hawkishness of the Federal Reserve and fears of Russian aggression in Eastern Europe, the mood on Wall Street feels like a return to the 1970s”.

Anis ChowdhuryStagflation in the 1970s

Worse, it seems few lessons have been learnt from the last stagflation episode. There is no agreed formal definition of stagflation, which refers to a combination of economic stagnation with high inflation, e.g., when unemployment and prices both rise.

When growth is weak and many are jobless, prices rarely rise, keeping inflation low. The converse is true when growth is strong. This inverse relationship between economic activity and inflation broke down with supply shocks, particularly oil and other primary commodity price surges during 1972-75.

Non-oil primary commodity prices on The Economist index more than doubled between mid-1972 and mid-1974. Prices of some commodities, e.g., sugar and urea fertilizer, rose more than five-fold!

As costlier energy pushed up production expenses, businesses raised prices and cut jobs. With higher food, fuel and other prices, rising costs, coupled with income losses, reduced aggregate demand, further slowing the economy.

Fed chokes economy to cut inflation

Years before becoming US Fed chair in 2006, a Ben Bernanke co-authored paper noted, “Looking more specifically at individual recessionary episodes associated with oil price shocks, we find that … oil shocks, per se, were not a major cause of these downturns”.

Jomo Kwame SundaramThey concluded, “an important part of the effect of oil price shocks on the economy results not from the change in oil prices, per se, but from the resulting tightening of monetary policy”. Their findings corroborated others, e.g., by James Tobin.

Following Milton Friedman and Anna Schwartz, other economists also found “in the postwar era there have been a series of episodes in which the Federal Reserve has in effect deliberately attempted to induce a recession to decrease inflation”.

The federal funds target rate rose from around 10% to nearly 20%, triggering an “extraordinarily painful recession”. Unemployment rose to nearly 11% nationwide – the highest in the post-war era – and as high as 17% in some states, e.g., Michigan, leaving long-term scars.

Interest rate hikes reduced needed investments. Outside the US economy, these sharp and rapid interest rate hikes triggered debt crises in Poland, Latin America, sub-Saharan Africa, South Korea and elsewhere.

Earlier open economic policies meant “the increase in world interest rates, the increased debt burden of developing countries, the growth slowdown in the industrial world…contributed to the developing countries’ stagnation”.

Countries seeking International Monetary Fund (IMF) financial support had to agree to severe fiscal austerity, liberalization, deregulation and privatization policy conditionalities. With per capita incomes falling and poverty rising, Latin America and Africa “lost two decades”.

Stagflation reprise

The IMF chief economist recently reiterated, “Inflation is a major concern”. The Bank of International Settlements has warned, “We may be reaching a tipping point, beyond which an inflationary psychology spreads and becomes entrenched.”

Central bankers’ anti-inflationary efforts mainly involve raising interest rates. This approach slows economies, accelerating recessions, often triggering debt crises without quelling rising prices due to supply shocks.

Economic recoveries from the 2008-09 global financial crisis (GFC) remained tepid for a decade after initially bold fiscal responses were quickly abandoned. Meanwhile, ‘quantitative easing’, other unconventional monetary policies and the Covid-19 pandemic raised debt to unprecedented levels.

GFC trade protectionist responses, US and Japanese ‘reshoring’ of foreign investment in China, the pandemic, the Ukraine war and sanctions against Russia and its allies have reversed earlier trade liberalization.

Higher interest rates in the rich North have triggered capital flight, causing developing country currencies to depreciate, especially against the US dollar. The slowing world economy has reduced demand for many developing country exports, while most migrant worker remittances decline.

Lessons not learned

Supply-side cost-push inflation is very different from the demand-pull variety. Without evidence, inflation ‘hawks’ insist that not acting urgently will be costlier later.

Acting too quickly against supply-shock inflation can be unwise. The 1970s’ energy crises sparked greater interest in energy efficiency. But higher interest rates in the 1980s deterred needed investments, even to reverse declining or stagnating productivity growth.

Raising interest rates also accelerated recessions. But similar commodity price rises before the 1970s’ and imminent stagflation episodes – involving energy and food respectively – obscure major differences.

For instance, ‘wage indexing’ – linking wage increases to price rises – enhanced the 1970s’ inflation spiral. But labour market deregulation since the 1980s has largely ended such indexation.

The IMF acknowledges globalization, ‘offshoring’ and labour-saving technical change have weakened unionization and workers’ bargaining power. With both elements of the 1970s’ wage-price spirals now insignificant, inflation is more likely to decline once supply bottlenecks ease.

But the wage-price spiral has also been replaced by a profit-price swirl. Reforms since the 1980s have also enhanced large corporations’ market power. Greater corporate discretion and reduced employees’ strength have thus increased profit shares, even during the pandemic.

Meanwhile, many more consumers struggle to meet their basic needs. Interest rate hikes have also hurt wage-earners, as falling labour shares of national income have been exacerbated by real wage stagnation, even contraction.

Hence, policymakers should ease supply bottlenecks and address imbalances to accelerate progress, not raise interest rates causing the converse. Thus, they should rein in corporate power, improve competition and protect the vulnerable.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.