SYDNEY, Jan 17 (IPS) – Inflation worries topped Ipsos’s What Worries the World survey in 2022 overtaking COVID concerns. The return of inflation caught major central banks, e.g., the US Federal Reserve (Fed), Bank of England, European Central Bank “off guard”. The persistence of inflation also surprised the International Monetary Fund (IMF). The return of inflation and its persistence exposed the poverty of the economics profession, unable to agree on its causes and required policy responses. It also exposed the profession’s anti-working class biases.

Anis Chowdhury

Inflation goof

Almost all major central banks as well as the IMF dismally failed to see the coming of inflation. In December 2020, the US Fed forecast that prices would rise by less than 2% in 2021 and 2022. It failed spectacularly when in December 2021, it estimated that inflation in 2022 would be just 2.6% even though prices were already rising by more than 5% a year.

The US Fed was not alone in failing to see inflation coming. The Governor of Australia’s central bank – the Reserve Bank of Australia (RBA) – was so confident of low inflation that he declared in March 2021 that the interest rate would remain at a historic low until at least 2024. Inflation in advanced economies during 2021 exceeded the average of forecasters’ expectations by around 5–8 percentage points. The IMF’s forecasts have badly and repeatedly undershot inflation.

There was a widespread view among most central bankers and leading economists that the price increases (or inflation) that began in mid-2021 were temporary, and price increases would slow or inflation would drift downwards in 2022. Some, of course, insisted otherwise, and wanted immediate anti-inflationary measures. Thus, policy confusion ruled.

Inflation phobia and dogma

Soon inflation phobia overtook and central banks were advised to act decisively with interest rate hikes even if it meant slowing the economy or a rise in unemployment. Exaggerated claims were made without evidence that not acting now would be more costly later.

The dogmatic inflation hawks ignored the fact that, in most cases, inflation does not accelerate to become harmful hyperinflation, but remains moderate. They also ignored their own neo-classical macroeconomic model, which suggests small welfare loss from moderate inflation.

Notwithstanding the IMF’s Article IV preamble which provides that economic policies should aim to foster “orderly economic growth with reasonable price stability, with due regard to circumstances”, a one-size-fits-all policy of steep interest rate hikes became the only medicine to be applied to achieve a universal inflation target of 2%, a figure plucked from thin air. Yet, central bankers and mainstream economists boast their credibility!

Inflation excuse for class war

Inflation is primarily an expression and outcome of conflicting claims over the distribution of national output and income, e.g., firms’ profit mark-ups vis-à-vis workers’ wages. Thus, no sooner inflation spiked early in the year due to slow adjustment of COVID-induced supply shortages to pent-up demand, exacerbated by war and sanctions, leading central bankers and mainstream economists found an excuse to weaponise economic policies against the working class.

Stoking the fear of wage-price spirals, they advocate the use of an interest rate sledgehammer to create unemployment and, in turn, discipline labour. This is despite research within the IMF and the Reserve Bank of Australia which found no evidence of wage-price spirals since the 1980s due to declines in labour’s bargaining power. Thus, Bloomberg headlined, “Fattest Profits Since 1950 Debunk Wage-Inflation Story of CEOs”.

Research conducted by the IMF also found increases in firms’ or corporations’ market power, resulting in higher prices and profit margins. Yet, the IMF does not think such factors “are contributing in any sizeable way to the current inflationary environment”. Instead, it justifies such fattening of profits on the ground that “they provide flexible buffers between general wage and general price increases” and that it is only a catching-up “after taking a hit in 2020”!

Labour is a clear loser. Labour’s income share in the GDP has been in decline since the early 1970s. Casualisation, off-shoring, anti-union legislation and technological progress have greatly reduced labour’s bargaining power, while privatisation and dilution of anti-monopoly legislation hugely strengthened corporate power and their collusive anti-competitive behaviour. Meanwhile, CEO compensation packages swelled to obnoxious levels, rising 940% since 1978 in the US as opposed to a 12% rise for workers during that period. Profiting from the pandemic, CEO pay increased by 16% in 2020 when workers suffered, and to a record level in 2021.

Leading central bankers and mainstream economists conveniently created a dogma around a 2% inflation target to justify their anti-labour stance. The 2% inflation target has become a global norm akin to the law of gravity, even though it has no theoretical or empirical basis. The law of gravity differs depending on altitude, but the 2% target is said to be universal regardless of circumstances!

Collateral damage

Meanwhile, the advanced countries’ inflation fight is causing adverse spillover into developing countries. Higher interest rates have slowed the world economy, and triggered capital outflows from developing countries, thereby depreciating their currencies and lowering their export earnings.

Together, these are causing devastating debt crises in many developing countries, similar to what happened in the 1980s. The rating agency S&P estimates that central bank rate rises could land global borrowers with US$8.6t in extra debt servicing costs in the coming years.

Meanwhile, the chiefs of the World Bank and the BIS urged “supply-side” policies professed to increase labour force participation and investment. These are code words for further labour market deregulation, privatisation and liberalisation.

The World Food Program has been active in Venezuela since last year, delivering bags of food to families of schoolchildren in some poor areas, such as remote areas accessed by river in the Arismedi municipality, in the southwestern plains state of Barinas. CREDIT: Gabriel Gómez/WFP

by Humberto Marquez (caracas)

Inter Press Service

CARACAS, Dec 15 (IPS) – The social crisis and humanitarian emergency in Venezuela became international headline news again once the government and the opposition, bitter adversaries for two decades, agreed to direct three billion dollars in state funds held abroad to social programs.

When the pact was signed on Nov. 26, renowned nutritionist Susana Raffalli published a photograph of the legs of a girl whose height is eight centimeters shorter than what is appropriate for her age. “I measured her today. Her growth has been irreversibly stunted,” she said.

“Between the first announcement of the social roundtable (meetings to that purpose were already held in 2014) and the one signed today in Mexico, a generation of Venezuelans like her was born. The agreement is not a trophy. It is a commitment to hope,” Raffalli stated.

The Social Agreement signed in Mexico “is an important contribution, which could mean urgent aid for children, the elderly, the disabled and indigenous people, whose situation is extremely critical,” Roberto Patiño, founder of Alimenta la Solidaridad, a network of soup kitchens for children, told IPS.

The resources involved in the agreement are Venezuelan state funds frozen in the United States and European nations that in 2019 refused to accept the re-election of President Nicolás Maduro, in power since 2013, adopted sanctions and recognized opposition lawmaker Juan Guaidó as president.

Now, in talks between the government and the opposition, with the mediation of governments from this region and Norway, an agreement was reached to unfreeze part of the funds and allocate them to social programs under United Nations supervision.

The United States and European countries are participating in the deal as sanctioning parties and the UN as manager of the released funds and social programs covered by them.

“These are absolutely insufficient resources in the face of the crisis, but well-managed they can have a positive impact given the country’s complex humanitarian emergency,” Piero Trepiccione, coordinator of the network of social centers in Latin America and the Caribbean run by the Catholic Jesuit order Society of Jesus, told IPS.

The HumVenezuela Platform, made up of dozens of civil society organizations, has maintained since 2019 that the social situation in this South American country is a complex humanitarian emergency, based on its records on food, water and sanitation, health, basic education and living conditions.

The sharp deterioration in the living conditions in this country over the last decade has gone hand in hand with the decline of the Venezuelan economy – a collapsed oil industry and several years of hyperinflation – whose most visible international consequence has been the migration of seven million Venezuelans.

Renowned nutritionist Susana Raffalli published, as an example of a generation of children born and growing up with malnutrition and other problems in Venezuela, a photograph of the legs of a girl who, the day the government-opposition agreement was reached, was eight centimeters shorter than the appropriate size for her age. CREDIT: Susana Rafalli/Twitter

Barrier against life

In recent years, U.S. sanctions and the political clash with other governments, as in the case of Colombia, a neighbor with which the borders and the transit of people and goods were closed, have had a major impact.

For example, tragedy struck the low-income family of Michel Saraí, a five-year-old girl with pneumonia who was treated at a small hospital in La Fría, a small town in the southwest near the border with Colombia, which lacked the equipment needed for the necessary tests and treatment.

When her health took a turn for the worse on Nov. 30, her parents decided not to take her to the public hospital in the regional capital, San Cristóbal, because they did not have the dozens of dollars charged there to accept patients, who must bring their own supplies and pay for tests.

A Civil Defense ambulance, with fuel donated by a neighbor – gasoline is scarce in the state of Táchira and others – took the girl and her mother some 25 kilometers to the border bridge in the town of Boca de Grita, so that she could be treated free of charge in the cities of Cúcuta or Puerto Santander, on the Colombian side.

With the border formally closed, the Colombian military agreed to receive the ambulance due to the emergency, but the Venezuelan National Guard refused to allow passage of the vehicle carrying the little girl connected to oxygen.

“We had no money to offer them to see if they would let her get through,” the father, Jonathan Pernía, told local reporters a few days later.

In desperation, the mother and an aunt accepted what seemed like the only alternative: disconnecting her from the oxygen, placing her on a wheelbarrow – “as if she were a sack of potatoes,” Pernía lamented – and running with her through the rain to the Colombian side of the bridge, where another ambulance was waiting for them. But the little girl arrived without vital signs.

At the morgue of the hospital in San Cristobal her parents picked up the body. A week later they were still trying to find the money needed to pay the burial expenses.

Jonathan Pernía, the impoverished father of a little girl who died when an ambulance was prevented from crossing the border between Venezuela and Colombia to give her emergency treatment, shows journalists the bill for the funeral expenses, which he has not been able to cover either. CREDIT: Courtesy of Bleima Márquez

Figures behind the crisis

In Venezuela, poverty – defined as those who cannot afford the basic food basket – currently affects 81.5 percent of the population (90.9 percent in 2021), according to the Living Conditions Survey of the Andrés Bello Catholic University, which surveyed 2300 households throughout the country. This is the first time in seven years that it has gone down, partly attributable to a rebound in the economy and remittances from migrants.

Meanwhile, multidimensional poverty – which takes into account housing, education, employment, services and income – fell from 65.2 percent in 2021 to 50.5 percent in 2022, and extreme poverty dropped from 68 percent in 2021 to 53.3 percent in 2022.

Venezuela is the most unequal country in the Americas, and along with Angola, Mozambique and Namibia is one of the most unequal in the world, as the richest 10 percent earn 70 times more (553.20 dollars per month on average) than the poorest 10 percent (7.90 dollars).

Seven million children are in school, down from 7.7 million in 2019, and an estimated 1.5 million children and adolescents are not in the educational system. Preschool and daycare coverage is just 56 percent.

The survey reported an improvement in formal employment and income this year, with average monthly earnings of 113 dollars for public employees, 142 dollars for the self-employed, and 150 dollars for people working in private sector companies.

As a consequence, food insecurity declined from 88 percent of Venezuelans worried about running out of food in 2021, to 78 percent, while the proportion of people who have gone a whole day without eating dropped to 14 percent, from 34 percent in 2021.

More than 90 percent of poor households have received food assistance from the government -especially carbohydrates- but only one third receive these products monthly.

In health, according to the survey, the use of public services is decreasing (70 percent) and health care is becoming more expensive because, while prices in private clinics are skyrocketing, 13 percent of those who turned to public services had to pay in outpatient clinics and 16 percent in hospitals, and in 65 percent of the cases they had to pay themselves for the medicine that was prescribed for them.

Venezuelan government and opposition negotiators, meeting in Mexico with that country’s Foreign Minister Marcelo Ebrard and Norwegian mediator Dag Nylander, agreed to help address social needs in their country, as a preliminary step to a possible agreement to solving the political crisis. CREDIT: National Assembly of Venezuela

Mexican formula

Jorge Rodríguez, president of the legislative National Assembly and the ruling party’s lead negotiator, said that with the funds released after the agreement reached in Mexico, the infrastructure and materials in 2300 schools will be covered, and the vaccines required in accordance with the World Health Organization (WHO) guidelines will be purchased.

Medicine for oncological and HIV patients will be obtained, radiotherapy programs, blood banks and at least 21 hospitals will be revived, while more than one billion dollars will be allocated to the national electricity grid.

The World Food Program (WFP), meanwhile, which now delivers food to families of 100,000 schoolchildren in poor areas in the north of the country, hopes to raise funds to provide meals to more than one million people by the end of 2023.

According to Trepiccione, of the Jesuit network, resources should be directed “to the recovery of the infrastructure of hospitals and schools, which are in terrible condition, because that generates a chain of jobs, services and economic activity along with the obvious improvements in the provision of health care and the quality of education.”

“The same can be said of reactivating the electrical system, hit by blackouts that affect above all the economy and the life of people in the western part of the country,” he added.

Patiño, from the network of soup kitchens, said priorities were “programs for early childhood care, pregnant women, school feeding, as well as care for the elderly and indigenous communities, segments where many are dying too young due to lack of urgent health care.”

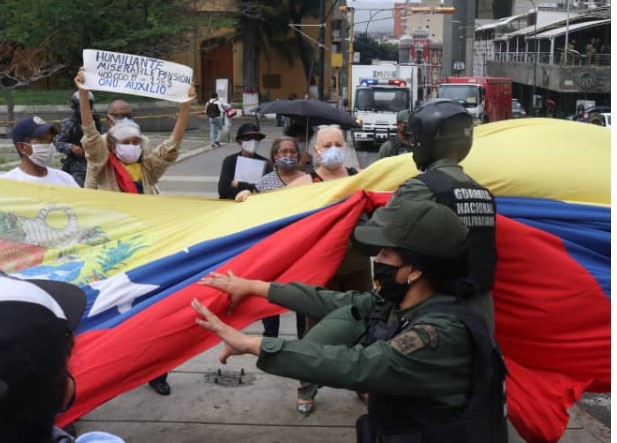

Groups of retirees and pensioners hold constant demonstrations in Caracas and other cities in protest against their tiny pensions, which in Venezuela are equal to the legal minimum wage and this December barely reached the equivalent of nine dollars for the entire month. CREDIT: Courtesy of Efecto Cocuyo

Government pensions, which are equal to the minimum wage, were equivalent to 30 dollars at the beginning of the year, but with the depreciation of the local currency they are equivalent to just nine dollars per month as of this December.

“We must also emphasize that this social agreement is absolutely insufficient in the face of the precarious conditions that exist in our country. These are resources that will be exhausted and the needs will not disappear,” said Patiño.

In his view, “the only thing that can really solve the crisis, the best possible social program, is a decent job, with a sufficient income and with a social security and public health program that takes care of the most needy.”

Funds for the agreement, frozen in banks in industrialized countries, will be released gradually under the supervision of a government-opposition committee and with UN agency management to tender, implement and oversee the programs, in 2023 and 2024.

And over the coming year new meetings will be held and further political agreements are expected, which may lead to an easing or lifting of sanctions and, eventually, to an improvement in the living conditions of Venezuela’s 28 million people.

Opinion by Jomo Kwame Sundaram (kuala lumpur, malaysia)

Inter Press Service

KUALA LUMPUR, Malaysia, Dec 13 (IPS) – Calls for more government regulation and intervention are common during crises. But once the crises subside, pressures to reform quickly evaporate and the government is told to withdraw. New financial fads and opportunities are then touted, instead of long needed reforms.

Global financial crisis

The 2007-2009 global financial crisis (GFC) began in the US housing market. Collateralized debt obligations (CDOs), credit default swaps (CDSs) and other related contracts, many quite ‘novel’, spread the risk worldwide, far beyond US mortgage markets.

Jomo Kwame Sundaram

Transnational financial ‘neural-like’ networks ensured vulnerability quickly spread to other economies and sectors, despite government efforts to limit contagion. As these were only partially successful, deleveraging – reducing the debt level by hastily selling assets – became inevitable, with all its dire consequences.

The GFC also exposed massive resource misallocations due to financial liberalization with minimal regulation of supposedly efficient markets. With growing arbitrage of interest rate differentials, achieving balanced equilibria has become impossible except in mainstream economic models.

Financialization has meant much greater debt and risk exposure as well as vulnerability for many households and firms, e.g., due to ‘term’ (duration) and currency ‘mismatches’, resulting in greater overall financial system fragility.

This has worsened global imbalances, reflected in larger trade and current account deficits and surpluses. In unfavourable circumstances, exposure of firms and households to risky assets and liabilities has been enough to trigger defaults.

Bold fiscal efforts succeeded in inducing modest economic recoveries before they were nipped in the bud soon after the ‘green shoots of recovery’ appeared. Instead, the US Fed initiated ‘unconventional’ monetary policies, offering easy credit with ‘quantitative easing’.

Currencies in flux

The seemingly coordinated rise of various, apparently unconnected asset prices cannot be explained by conventional economics. Thus, speculation in commodity, currency and stock markets has been grudgingly acknowledged as worsening the GFC.

The exchange rates of many currencies have also come under greater pressure as residents borrowed in low interest rate currencies such as the Japanese yen. In turn, they have typically bought financial assets promising higher returns.

Thus, higher interest rates attract capital inflows, raising most domestic asset prices. Exchange rate movements are supposed to reflect comparative national economic strengths, but rarely do so. But conventional monetary responses worsen, rather than mitigate, contractionary tendencies.

Globalization of trade and finance has generated contradictory pressures. All countries are under pressure to generate trade or current account surpluses. But this, of course, is impossible as not all economies can run surpluses simultaneously.

Many try to do so by devaluing their currencies or cutting costs by other means. But only the US can use its ‘exorbitant privilege’ to maintain both budgetary and current account deficits by simply issuing Treasury bonds.

Currency markets can also undermine such efforts by enabling arbitrage on interest rate differentials. International imbalances have worsened, as seen in larger current account deficits and surpluses.

Contrary to mainstream economics, currency speculation does not equilibrate national, let alone international markets. It does not reflect economic fundamentals, ensuring exchange rate volatility, to damaging effect.

Commodity speculation

Thanks to currency mismatches, many companies and households face greater risk. Exchange rate fluctuations, in turn, exacerbate price volatility and its harmful consequences, which vary with circumstances.

Changes in ‘fundamentals’ no longer explain commodity price volatility. Meanwhile, more commodity speculation has resulted in greater price volatility and higher prices for food, oil, metals and other raw materials.

These prices have been driven by much more speculation, often involving indexed funds trading in real assets. The resulting price volatility especially affects everyone, as food consumers, and developing countries’ agricultural producers.

Sharp increases in commodity prices since mid-2007 were largely driven by speculation, mainly involving indexed funds. With the Great Recession following the GFC, most commodity producers in developing countries faced difficulties.

Since then, nearly all commodity prices fell from the mid-2010s as the world economic slowdown showed no sign of abating until economic sanctions in 2022 pushed up food, energy, fertilizer and other prices once again.

Besides hurting export revenues, lower commodity prices and even greater volatility have accelerated depreciation of earlier investments in equipment and infrastructure following the commodity price spikes.

Integrated solutions needed

The uneven financial system meltdown following the GFC raised expectations that ‘finance-as-usual’ would never return. But lasting solutions to threats, such as currency and commodity speculation, require international cooperation and regulation.

Meanwhile, goods and financial markets have become more interconnected. Thus, a truly multilateral and cooperative approach has to be found in the complex interconnections involving international trade and finance.

In this asymmetrically interdependent world, policy reforms are urgently needed. All countries need to be able to pursue appropriate countercyclical macroeconomic policies. Also, small economies should be able to achieve exchange rate stability at affordably low cost.

Although prompt actions were undertaken in response to the GFC, the world economy experienced a protracted slowdown, the ‘Great Recession’. Myopic policymakers in most developed economies focus on perceived national risks, ignoring international ones, especially those affecting developing countries.

Contrary to widespread popular presumption, the Bretton Woods multilateral monetary and financial arrangements did not include a regulatory regime. Nor has such a regime emerged since, even after US President Nixon unilaterally ended the Bretton Woods system in 1971.

With the gagged voice of developing countries in international financial institutions and markets, the United Nations must lead, as it did in the mid-1940s.

It is the only world institution which could legitimately develop a better alternative. Thankfully, the UN Charter assigns it responsibility to lead efforts to do so.

Opinion by Jomo Kwame Sundaram, Ndongo Samba Sylla (dakar and kuala lumpur)

Inter Press Service

DAKAR and KUALA LUMPUR, Nov 22 (IPS) – The ongoing plunder of Africa’s natural resources drained by capital flight is holding it back yet again. More African nations face protracted recessions amid mounting debt distress, rubbing salt into deep wounds from the past.

With much less foreign exchange, tax revenue, and policy space to face external shocks, many African governments believe they have little choice but to spend less, or borrow more in foreign currencies.

Ndongo Samba Sylla

Most Africans are struggling to cope with food and energy crises, inflation, higher interest rates, adverse climate events, less health and social provisioning. Unrest is mounting due to deteriorating conditions despite some commodity price increases.

Economic haemorrhage

After ‘lost decades’ from the late 1970s, Africa became one of the world’s fastest growing regions early in the 21st century. Debt relief, a commodity boom and other factors seemed to support the deceptive ‘Africa rising’ narrative.

According to the High Level Panel on Illicit Financial Flows from Africa, the continent was losing over $50 billion annually. This was mainly due to ‘trade mis-invoicing’ – under-invoicing exports and over-invoicing imports – and fraudulent commercial arrangements.

Transnational corporations (TNCs) and criminal networks account for much of this African economic surplus drain. Resource-rich countries are more vulnerable to plunder, especially where capital accounts have been liberalized.

Jomo Kwame Sundaram

Externally imposed structural adjustment programs (SAPs), after the early 1980s’ sovereign debt crises, have forced African economies to be even more open – at great economic cost. SAPs have made them more (food) import-dependent while increasing their vulnerability to commodity price shocks and global liquidity flows.

Leonce Ndikumana and his colleagues estimate over 55% of capital flight – defined as illegally acquired or transferred assets – from Africa is from oil-rich nations, with Nigeria alone losing $467 billion during 1970-2018.

Over the same period, Angola lost $103 billion. Its poverty rate rose from 34% to 52% over the past decade, as the poor more than doubled from 7.5 to 16 million.

Oil proceeds have been embezzled by TNCs and Angola’s elite. Abusing her influence, the former president’s daughter, Isabel dos Santos acquired massive wealth. A report found over 400 companies in her business empire, including many in tax havens.

From 1970 to 2018, Côte d’Ivoire lost $55 billion to capital flight. Growing 40% of the world’s cocoa, it gets only 5–7% of global cocoa profits, with farmers getting little. Most cocoa income goes to TNCs, politicians and their collaborators.

Mining giant South Africa (SA) has lost $329 billion to capital flight over the last five decades. Mis-invoicing, other modes of embezzling public resources, and tax evasion augment private wealth hidden in offshore financial centres and tax havens.

Fiscal austerity has slowed job growth and poverty reduction in ‘the most unequal country in the world’. In SA, the richest 10% own over half the nation’s wealth, while the poorest 10% have under 1%!

Resource theft and debt

With this pattern of plunder, resource-rich African countries – that could have accelerated development during the commodity boom – now face debt distress, depreciating currencies and imported inflation, as interest rates are pushed up.

Zambia’s default on its foreign debt obligations in late 2020 has made headlines. But foreign capture of most Zambian copper export proceeds is not acknowledged.

During 2000-2020, total foreign direct investment income from Zambia was twice total debt servicing for external government and government-guaranteed loans. In 2021, the deficit in the ‘primary income’ account (mainly returns to capital) of Zambia’s balance of payments was 12.5% of GDP.

As interest payments on public external debt came to ‘only’ 3.5% of GDP, most of this deficit (9% of GDP) was due to profit and dividend remittances, as well as interest payments on private external debt.

For the IMF, World Bank and ‘creditor nations’, debt ‘restructuring’ is conditional on continuing such plunder! African countries’ worsening foreign indebtedness is partly due to lack of control over export earnings controlled by TNCs, with African elite support.

Resource pillage, involving capital flight, inevitably leads to external debt distress. Invariably, the IMF demands government austerity and opening African economies to TNC interests. Thus, we come full circle, and indeed, it is vicious!

Africa’s wealth plunder dates back to colonial times, and even before, with the Atlantic trade of enslaved Africans. Now, this is enabled by transnational interests crafting international rules, loopholes and all.

Such enablers include various bankers, accountants, lawyers, investment managers, auditors and other wheeler dealers. Thus, the origins of the wealth of ‘high net-worth individuals’, corporations and politicians are disguised, and its transfer abroad ‘laundered’.

What can be done?

Capital flight is not mainly due to ‘normal’ portfolio choices by African investors. Hence, raising returns to investment, e.g., with higher interest rates, is unlikely to stem it. Worse, such policy measures discourage needed domestic investments.

Besides enforcing efficient capital controls, strengthening the capabilities of specialized national agencies – such as customs, financial supervision and anti-corruption bodies – is important.

African governments need stronger rules, legal frameworks and institutions to curb corruption and ensure more effective natural resource management, e.g., by revising bilateral investment treaties and investment codes, besides renegotiating oil, gas, mining and infrastructure contracts.

Records of all investments in extractive industries, tax payments by all involved, and public prosecution should be open, transparent and accountable. Punishment of economic crimes should be strictly enforced with deterrent penalties.

The broader public – especially civil society organizations, local authorities and impacted communities – must also know who and what are involved in extractive industries.

Only an informed public who knows how much is extracted and exported, by whom, what revenue governments get, and their social and environmental effects, can keep corporations and governments in check.

Improving international trade and finance transparency is essential. This requires ending banking secrecy and better regulation of TNCs to curb trade mis-invoicing and transfer pricing, still enabling resource theft and pillage.

OECD rhetoric has long blamed capital flight on offshore tax havens on remote tropical islands. But those in rich countries – such as the UK, US, Switzerland, Netherlands, Singapore and others – are the biggest culprits.

Stopping haemorrhage of African resource plunder by denying refuge for illicit transfers should be a rich country obligation. Automatic exchange of tax-related information should become truly universal to stop trade mis-invoicing, transfer pricing abuses and hiding stolen wealth abroad.

Unitary taxation of transnational corporations can help end tax abuses, including evasion and avoidance. But the OECD’s Inclusive Framework proposals favour their own governments and corporate interests.

Africa is not inherently ‘poor’. Rather, it has been impoverished by fraud and pillage leading to resource transfers abroad. An earnest effort to end this requires recognizing all responsibilities and culpabilities, national and international.

Africa’s veins have been slit open. The centuries-long bleeding must stop.

Dr Ndongo Samba Sylla is a Senegalese development economist working at the Rosa Luxemburg Foundation in Dakar. He authored The Fair Trade Scandal. Marketing Poverty to Benefit the Rich and co-authored Africa’s Last Colonial Currency: The CFA Franc Story. He also edited Economic and Monetary Sovereignty for 21st century Africa, Revolutionary Movements in Africa and Imperialism and the Political Economy of Global South’s Debt. He tweets at @nssylla

Opinion by Jomo Kwame Sundaram, Anis Chowdhury (sydney and dakar)

Inter Press Service

SYDNEY and DAKAR, Nov 01 (IPS) – Developing countries have long been told to avoid borrowing from central banks (CBs) to finance government spending. Many have even legislated against CB financing of fiscal expenditure.

Central bank fiscal financing

Such laws are supposedly needed to curb inflation – below 5%, if not 2% – to accelerate growth. These arrangements have also constrained a potential CB developmental role and government ability to respond better to crises.

Anis ChowdhuryImproved monetary-fiscal policy coordination is also needed to achieve desired structural transformation, especially in decarbonizing economies. But too many developing countries have tied their own hands with restrictive legislation.

A few have pragmatically suspended or otherwise circumvented such self-imposed prohibitions. This allowed them to borrow from CBs to finance pandemic relief and recovery packages.

Such recent changes have re-opened debates over the urgent need for counter-cyclical and developmental fiscal-monetary policy coordination.

Monetary financing rubbished

But financial interests claim this enables national CBs to finance government deficits, i.e., monetary financing (MF). MF is often blamed for enabling public debt, balance of payments deficits, and runaway inflation.

As William Easterly noted, “Fiscal deficits received much of the blame for the assorted economic ills that beset developing countries in the 1980s: over indebtedness and the debt crisis, high inflation, and poor investment performance and growth”.

Hence, calls for MF are typically met with scepticism, if not outright opposition. MF undermines central bank independence (CBI) – hence, the strict segregation of monetary from fiscal authorities – supposedly needed to prevent runaway inflation.

Jomo Kwame SundaramRecent International Monetary Fund (IMF) research insists MF “involves considerable risks”. But it acknowledges MF to cope with the pandemic did not jeopardize price stability. A Bank of International Settlements paper also found MF enabled developing countries to respond countercyclically to the pandemic.

Cases of MF leading to runaway inflation have been very exceptional, e.g., Bolivia in the 1980s or Zimbabwe in 2007-08. These were often associated with the breakdown of political and economic systems, as when the Soviet Union collapsed.

Bolivia suffered major external shocks. These included Volcker’s interest rate spikes in the early 1980s, much reduced access to international capital markets, and commodity price collapses. Political and economic conflicts in Bolivian society hardly helped.

Similarly, Zimbabwe’s hyperinflation was partly due to conflicts over land rights, worsened by government mismanagement of the economy and British-led Western efforts to undermine the Mugabe government.

Indian lessons

Former Reserve Bank of India Governor Y.V. Reddy noted fiscal-monetary coordination had “provided funds for development of industry, agriculture, housing, etc. through development financial institutions” besides enabling borrowing by state owned enterprises (SOEs) in the early decades.

For him, less satisfactory outcomes – e.g., continued “macro imbalances” and “automatic monetization of deficits” – were not due to “fiscal activism per se but the soft-budget constraint” of SOEs, and “persistent inadequate returns” on public investments.

Monetary policy is constrained by large and persistent fiscal deficits. For Reddy, “undoubtedly the nature of interaction between depends on country-specific situation”.

Reddy urged addressing monetary-fiscal policy coordination issues within a broad common macroeconomic framework. Several lessons can be drawn from Indian experience.

First, “there is no ideal level of fiscal deficit, and critical factors are: How is it financed and what is it used for?” There is no alternative to SOE efficiency and public investment project financial viability.

Second, “the management of public debt, in countries like India, plays a critical role in development of domestic financial markets and thus on conduct of monetary policy, especially for effective transmission”.

Third, “harmonious implementation of policies may require that one policy is not unduly burdening the other for too long”.

Lessons from China?Zhou Xiaochuan, then People’s Bank of China (PBoC) Governor, emphasized CBs’ multiple responsibilities – including financial sector development and stability – in transition and developing economies.

China’s CB head noted, “monetary policy will undoubtedly be affected by balance of international payments and capital flows”. Hence, “macro-prudential and financial regulation are sensitive mandates” for CBs.

PBoC objectives – long mandated by the Chinese government – include maintaining price stability, boosting economic growth, promoting employment, and addressing balance of payments problems.

Multiple objectives have required more coordination and joint efforts with other government agencies and regulators. Therefore, “the PBoC … works closely with other government agencies”.

Zhou acknowledged, “striking the right balance between multiple objectives and the effectiveness of monetary policy is tricky”. By maintaining close ties with the government, the PBoC has facilitated needed reforms.

He also emphasized the need for policy flexibility as appropriate. “If the central bank only emphasized keeping inflation low and did not tolerate price changes during price reforms, it could have blocked the overall reform and transition”.

During the pandemic, the PBoC developed “structural monetary” policy tools, targeted to help Covid-hit sectors. Structural tools helped keep inter-bank liquidity ample, and supportive of credit growth.

More importantly, its targeted monetary policy tools were increasingly aligned with the government’s long-term strategic goals. These include supporting desired investments, e.g., in renewable energy, while preventing asset price bubbles and ‘overheating’.

In other words, the PBoC coordinates monetary policy with fiscal and industrial policies to achieve desired stable growth, thus boosting market confidence. As a result, inflation in China has remained subdued.

Needed reforms

Effective fiscal-monetary policy coordination needs appropriate arrangements. An IMF working paper showed, “neither legal independence of central bank nor a balanced budget clause or a rule-based monetary policy framework … are enough to ensure effective monetary and fiscal policy coordination”.

Appropriate institutional and operational arrangements will depend on country-specific circumstances, e.g., level of development and depth of the financial sector, as noted by both Reddy and Zhou.

When the financial sector is shallow and countries need dynamic structural transformation, setting up independent fiscal and monetary authorities is likely to hinder, not improve stability and sustainable development.

Understanding each other’s objectives and operational procedures is crucial for setting up effective coordination mechanisms – at both policy formulation and implementation levels. Such an approach should better achieve the coordination and complementarity needed to mutually reinforce fiscal and monetary policies.

Coherent macroeconomic policies must support needed structural transformation. Without effective coordination between macroeconomic policies and sectoral strategies, MF may worsen payments imbalances and inflation. Macro-prudential regulations should also avoid adverse MF impacts on exchange rates and capital flows.

Poorly accountable governments often take advantage of real, exaggerated and imagined crises to pursue macroeconomic policies for regime survival, and to benefit cronies and financial supporters.

Undoubtedly, much better governance, transparency and accountability are needed to minimize both immediate and longer-term harm due to ‘leakages’ and abuses associated with increased government borrowing and spending.

Citizens and their political representatives must develop more effective means for ‘disciplining’ policy making and implementation. This is needed to ensure public support to create fiscal space for responsible counter-cyclical and development spending.

NEW YORK, Oct 26 (IPS) – Held in-person for the first time in three years, the annual meetings of the International Monetary Fund and World Bank last week in Washington, D.C. failed to offer solutions to the dozens of developing countries in debt distress or on the forewarned global recession instigated by monetary tightening.

Meanwhile, austerity measures are reinforced through a repeated emphasis on fiscal tightening, underpinned by a monetarism upheld by the IMF and rich country central banks.

The scenario of a dual tightening in both monetary and fiscal policy is only exacerbated by the absence of political will among creditors to cooperate in debt restructuring, bolstered by narratives of losing market access to financial flows.

New loan programs are created by the IMF to boost concessional financing for food price shocks, climate transitions and liquidity shortfalls. However, these very loans create new debt and reinscribe the very austerity measures that worsen the challenges of inflation and climate.

Within these asymmetries of power and access in the world economy, and the foreclosing of developmental policy tools for developing countries, what then is the fate of the vast majority of people and nations in the world?

The IMF’s World Economic Outlook warned of an imminent recession amidst a shift of financial regime from cheap and easy money to an aggressive synchronization of global monetary tightening.

“In short, the worst is yet to come, and for many people 2023 will feel like a recession,” said IMF Chief Economist Pierre-Olivier Gourinchas. Convening the world’s finance ministers, central bank governors, and financial market leaders, the IMF announced a slowdown in global growth by 2.7%, down from the 3.2% growth projected for this year.

On the heels of a global pandemic followed by the war in Ukraine, the US Federal Reserve’s interest rate hikes, aimed toward domestic price stability, is creating a global push toward more expensive money.

A stronger dollar, higher international and domestic interest rates, coupled with depreciating currencies and sell-offs in many developing country assets, is generating protracted economic and social pain across the globe.

The spillover impacts are seen in soaring food and fuel prices, increases in dollar-denominated debt and imports costs, volatile commodity markets and debt distress intensifying into a 50-year record across the developing world.

The UN’s 2022 Trade and Development Report warns that the most vulnerable countries and communities are being hit the hardest. Warnings of another ‘lost decade’ abound, in that the current interest rate hikes resemble those of 1979-82, which triggered debt crises in over 40 developing countries where ‘structural adjustment programs’ through IMF loans contributed to a decade of lost growth and development across the Global South.

The tightrope global central banks are walking is acknowledged by IMF Managing Director, Kristalina Georgieva, who says, “Not tightening enough would cause inflation to become de-anchored and entrenched — which would require future interest rates to be much higher and more sustained, causing massive harm on growth and massive harm on people.

On the other hand, tightening monetary policy too much and too fast — and doing so in a synchronized manner across countries — could push many economies into prolonged recession.”

Meanwhile, the topline recommendation of the IMF’s Global Financial and Stability Report is that “central banks must act resolutely to bring inflation back to target.” Doing otherwise would risk credibility and market volatility, or in other words, create difficulties in market access to financial and investment flows and/or worsen borrowing terms.

One of the central tenets of neoclassical economic consensus among global central banks is that of maintaining price stability through a low inflation target of 2%. Financial rulemakers have for decades deemed inflation a threat to economic growth by way of the specter of hyperinflation. However, empirical evidence points to the contrary.

Collating data from 31 countries from 1961-94, World Bank chief economist Michael Bruno and William Easterly concluded that the inflation does not lead to lower growth, even when the significant oil price increase of 1974-75 is included.

The US Federal Reserve’s own historical archives demonstrate that the so-called ‘Great Inflation’ of 1965-82 did not harm growth either. In light of these studies by neoclassical economists and central bank institutions, economists Anis Chowdhury and Jomo Kwame Sundaram argue that “there is no empirical basis for setting a particular threshold, such as the now standard 2% inflation target – long acknowledged as ‘plucked from the air.’”

From press conferences to panel speeches, the IMF leadership repeats that the danger of “entrenched” inflation requires a global commitment to tackle it head on through global to domestic monetary tightening.

This stems in large part from a belief that once inflation begins, it has an inherent tendency to accelerate. Consequently, IMF loans and surveillance recommend central bank independence (from the executive) as a means to ensure unbiased financial policymaking, while critics contend that it has only enhanced the influence and power of big banks and financial actors, largely at the expense of the real economy.

However, history again demonstrates that inflation does not accelerate easily, even when workers have more bargaining power, or wages are indexed to consumer prices – as in some countries.

Lost decade redux?

The IMF’s Fiscal Monitor, published on October 12, called upon all policymakers to “maintain a tight fiscal stance, so that fiscal policy does not work at cross-purposes with monetary policy.” In essence, fiscal policy must serve monetary policy in its “fight against inflation,” by retrenching public spending for the singular objective of sending “a powerful signal that policymakers are aligned in the fight against inflation.”

The rationale is straightforward: “In a time of high inflation, policies to address high food and energy prices should not add to aggregate demand.” Increased demand is anathema, as it “forces central banks to raise interest rates even higher.”

The fiscal tightening is not new. In 2021, 131 governments started scaling back public spending. The geographic and population scale of austerity cuts is expected to intensify up to 2025.

Governments are implementing, or discussing, a range of fiscal adjustment policies, such as targeting social protection, regressive taxation, reducing public expenditure in social sectors, eliminating subsidies, privatizing public services or State-Owned Enterprises, pension reforms, labor flexibilization.

All have long histories of negative social impacts on economic and social rights, such as the right to food, water, health, housing, education, and livelihoods. The human impact will reach over 6 billion people, or 85% of humanity, in 2023.

In a time of poly-crisis, retrenching public spending and imposing regressive taxes that disproportionately hurt the poor, especially women, not only extinguishes the hope of achieving the Sustainable Development Goals by 2030, but more fundamentally, regresses decades of fighting poverty.

Meanwhile, the IMF’s Board has approved the creation of two new loan facilities, the new Food Shock Window, available for a year to countries reeling from the global food price crisis, and the Resilience and Sustainability Trust (RST), through which many rich countries may re-channel their unused Special Drawing Rights if the funds are used to address “external shocks, including climate change and pandemics” by rules set out by the Fund.

While both loans address urgent threats, they also create new debt. The RST is also conditional upon an IMF loan program hinged on fiscal consolidation.

The severity of the food crisis warrants aid in the form of grants not loans. Based on prior research done by the World Bank and Center for Global Development on food price spikes, Oxfam estimates that another 65 million people could be pushed below the $1.90 extreme poverty line as a consequence of food price increases.

Debt crises nearing point of no return

Despite the imminent threat of a debt crises imploding across many developing countries, sovereign debt solutions, the Group of 20, IMF, World Bank as well as the Institute of International Finance, the consortium of private financial actors, have to date failed to create viable solutions.

The G20’s Debt Service Suspension Initiative, which suspended debt payments for 73 low-income countries, was terminated at the end of 2021. And two years after the Common Framework was established in 2020, it’s multiple flaws have led even the World Bank to call it a ‘slow-motion debt tragedy.’

One key dilemma is the lack of political will to enforce a comparability of treatment, where all creditors, including private, participate on equivalent terms or restructuring and in the principle of burden sharing. Another challenge is the glacial pace of restructuring is not only protracted but also riddled with uncertainty.

Middle-income countries, where the vast majority of the world’s poor reside and where serious debt defaults are taking place, are not included. Low-income countries fear that access to commercial financing will be cut off if they apply to the Common Framework, as evidenced by Fitch and S&P slashed Ethiopia’s sovereign rating when the nation applied to the Common Framework in 2021.

Out of the three countries that have so far asked for their debt to be treated – Chad, Ethiopia and Zambia – only Zambia has seen some forward movement.

The narratives coming from within the IMF reiterate a subservience to market access and creditor interests. Across panels and webinars, senior level IMF staff remarked that a large debt restructuring is a serious event, which may result in a decrease of future multilateral and private financing, in amounts that outweigh the financing gained in relief or restructuring.

Some warned that private creditors will not participate in debt restructuring where national fiscal instability reigns. To secure market access, countries have to tighten fiscal belts even more. The logic here is that financial stability imperative for accessing private credit requires fiscal consolidation that generates social devastation.

The lack of official creditor participation and the dilemma of transparency, referring in large part to China, was repeatedly stressed as a key problem. At the same time, an old and wholly condescending trope of the need to increase debtor discipline in light of its financial mismanagement and irresponsibility repeatedly emerged.

Meanwhile, there is no mention of the often-legalized corruption of private actors, such as tax evasion and avoidance, speculative and/or rigged trading. Amidst the talk, actual debt solutions are in omission. While political will is already in short supply, the lack of cooperation toward problem-solving is exacerbated by the finger-pointing between the creditor groups of bilateral, private, and multilateral.

History has repeatedly illustrated the way forward on debt, and the waves of austerity that it generates. For decades, advocates and policymakers alike have called for a transparent and binding debt workout mechanism within a multilateral framework for debt crisis resolution, in a process convening all creditors.

The UN General Assembly has adopted multiple resolutions calling for such a mechanism over the years. Debt justice movements from across the developing world have urged for the cancellation of all unsustainable and illegitimate debts in a manner that is ambitious, unconditional, and without repercussions for future market access.

Past cases show how reducing debt stock and payments allow for countries to increase their public financing for urgent domestic needs.

The principle of burden-sharing ensures genuine debt relief, as does the commitment to include all creditors in an automatic or orderly way. Recognizing that multilateral institutions account for around one-third of the outstanding debt of low- and lower-middle-income countries, the World Bank and IMF must participate in such efforts.

They should both cancel debt payments owed, and the IMF should eliminate surcharges. Protection needs to be provided to debtor states against holdouts and lawsuits by non-participating creditors, while laws and procedures for responsible borrowing and lending need to be ensured to protect citizens and communities against corrupt, predatory and odious debts.

Last but not least, an automatic mechanism for a debt standstill in the wake of an extreme exogenous shock should be created. As proposed by the G77 group of developing countries in the UN General Assembly in response to the global financial crisis of 2007-8, such a mechanism must “be established for a determined period in response to external catastrophe events, as climate and natural disasters, health pandemic, military conflict and inflation.” The prescience of the G77 group in 2009 offers a salient message.

While the developing world has little recourse but to ‘dance to the tune of the Federal Reserve,’ the devastating toll of the human, social and economic crisis must be addressed through tools and choices that can be generated.

The question is how to muster political will, be it from the moral pressure of global justice movement to analysis of the effects that soaring poverty and intensifying climate change will have on the very survival of our planet and species.

Bhumika Muchhala is development economist and senior advocate on economic governance at Third World Network. She works on research, analysis, advocacy and public education on the international political economy of development, feminist economics and decolonial theory and approaches.

Opinion by Jomo Kwame Sundaram, Anis Chowdhury (sydney and kuala lumpur)

Inter Press Service

SYDNEY and KUALA LUMPUR, Oct 25 (IPS) – Widespread adverse reactions to the UK government’s recent ‘mini-budget’ forced new Prime Minister Liz Truss to resign. The episode highlighted problems of macroeconomic policy coordination and the interests involved.

Macro-policy coordination

But macroeconomic, specifically fiscal-monetary policy coordination almost became “taboo” as central bank independence (CBI) became the new orthodoxy. It has been accused of enabling CBs to finance government deficits. Critics claim inflation, even hyperinflation, becomes inevitable.

Anis ChowdhuryGovernment finance ministries and CBs are the two main macroeconomic policy protagonists. Poor ‘macro-policy’ coordination has generated problems, including contradictory policy responses. This has meant more macroeconomic and financial instability, worrying markets and investors.

Fiscal policy – notably variations in government tax and spending – mainly aims to influence long-term growth and distribution. CB monetary policy – e.g., variations in short-term interest rates and credit growth – claims to prioritize price and exchange rate stability.

By the early 1990s, the ‘Washington consensus’ implied the two macro-policy actors should work independently due to their different time horizons. After all, governments are subject to short-term political considerations inimical to monetary stability needed for long-term growth.

Claiming to be “technocratic”, CBs have increasingly set their own goals or targets. CBI has involved both ‘goal’ and ‘instrument’ independence, instead of ‘goal dependence’ with ‘instrument independence’.

CBI was ostensibly to avoid ‘fiscal dominance’ of monetary policy. Meanwhile, government fiscal policy became subordinated to CB inflation targets. For former Reserve Bank of Australia Deputy Governor Guy Debelle, monetary policy became “the only game in town for demand management”.

Debelle noted that except for rare and brief coordinated fiscal stimuli in early 2009, after the onset of the global financial crisis, “demand management continued to be the sole purview of central banks. Fiscal policy was not much in the mix”.

Jomo Kwame SundaramSub-optimal outcomes

But more than three decades of “divorce” between independent CBs and fiscal authorities have failed to deliver its promised benefits. Instead, monetary policy dominance has worsened financial instability.

Adam Posen found the costs of disinflation, or keeping inflation low, higher in OECD countries with CBI. Carl Walsh found likewise in the European Community.

For Guy Debelle and Stanley Fischer, CBs have sought to enhance their credibility by being tougher on inflation, even at the expense of output and employment losses.

Committed to arbitrary targets, independent CBs have sought credit for keeping inflation low. They deny other contributory factors, e.g., labour’s diminished bargaining power and globalization, particularly cheaper supplies.

John Taylor, author of the ‘Taylor rule’ CB mantra, concluded CB “performance was not associated with de jure central bank independence”. De jure CB independence has not prevented them from “deviating from policies that lead to both price and output stability”.

The de facto independent US Fed has also taken “actions that have led to high unemployment and/or high inflation”. As single-minded independent CBs pursued low inflation, they neglected their responsibility for financial stability.

CBs’ indiscriminate monetary expansion during the 2000s’ Great Moderation enabled asset price bubbles and dangerous speculation, culminating in the global financial crisis (GFC).

Since the GFC, “the financial sector has become dependent on easy liquidity… To compensate for quantitative easing (QE)-induced low return…, increased the risk profile of their other assets, taking on more leverage, and hedging interest rate risk with derivatives”.

Independent CBs also never acknowledge the adverse distributional consequences of their policies. This has been true of both conventional policies, involving interest rate adjustments, and unconventional ones, with bond buying, or QE. All have enabled speculation, credit provision and other financial investments.

They have also helped inefficient and uncompetitive ‘zombie’ enterprises survive. Instead of reversing declining long-term productivity growth, the slowdown since the GFC “has been steep and prolonged”.

Dire consequences

The pandemic has seen unprecedented fiscal and monetary responses. But there has been little coordination between fiscal and monetary authorities. Unsurprisingly, greater pandemic-induced fiscal deficits and monetary expansion have raised inflationary pressures, especially with supply disruptions.

This could have been avoided if policymakers had better coordinated fiscal and monetary measures to unlock key supply bottlenecks. War and economic sanctions have made the supply situation even more dire.

Government debt has been rising since the GFC, reaching record levels due to pandemic measures. CBs hiking interest rates to contain inflation have thus worsened public debt burdens, inviting austerity measures.

Thus, countries go through cycles of debt accumulation and output contraction. Supposed to contain inflation, they adversely impact livelihoods. Many more developing countries face debt crises, further setting back progress.

Needed reforms

Sixty years ago, Milton Friedman asserted, “money is too important to be left to the central bankers”. He elaborated, “One economic defect of an independent central bank … is that it almost invariably involves dispersal of responsibility… Another defect … is the extent to which policy is … made highly dependent on personalities… third … defect is that an independent central bank will almost invariably give undue emphasis to the point of view of bankers”.

Thus, government-sceptic Friedman recommended, “either to make the Federal Reserve a bureau in the Treasury under the secretary of the Treasury, or to put the Federal Reserve under direct congressional control.

“Either involves terminating the so-called independence of the system… either would establish a strong incentive for the Fed to produce a stabler monetary environment than we have had”.

Undoubtedly, this is an extreme solution. Friedman also suggested replacing CB discretion with monetary policy rules to resolve the problem of lack of coordination. But, as Alan Blinder has observed, such rules are “unlikely to score highly”.

Effective fiscal-monetary policy coordination requires appropriate supporting institutions and operating arrangements. As IMF research has shown, “neither legal independence of central bank nor a balanced budget clause or a rule-based monetary policy framework … are enough to ensure effective monetary and fiscal policy coordination”.

Although rules-based policies may enhance transparency and strengthen discipline, they cannot create “credibility”, which depends on policy content, not policy frameworks.

For Debelle, a combination of “goal dependence” and “instrument or operational independence” of CBs under strong democratic or parliamentary oversight may be appropriate for developed countries.

There is also a need to broaden membership of CB governing boards to avoid dominance by financial interests and to represent broader national interests.

But macro-policy coordination should involve more than merely an appropriate fiscal-monetary policy mix. A more coherent approach should also incorporate sectoral strategies, e.g., public investment in renewable energy, education & training, healthcare. Such policy coordination should enable sustainable development and reverse declining productivity growth.

As Buiter urges, it is up to governments “to make appropriate use of … fiscal space” created by fiscal-monetary coordination. Democratic checks and balances are needed to prevent “pork-barrelling” and other fiscal abuses and to protect fiscal decision-making from corruption.

Opinion by Isabel Ortiz, Matti Kohonen (london / new york)

Inter Press Service

LONDON / NEW YORK, Oct 24 (IPS) – Finance ministers of the G20 and the world met in Washington, October 10-16, to discuss how to navigate multiple crises, including rising cost-of-living, broken global supply chains, climate shocks, and the lingering COVID-19 pandemic.

All this weighted heavily on the IMF outlook, pointing to a bleak future ahead.

This is particularly bad news for developing countries. Using IMF data, our research showed that recovery spending in the last two years of the pandemic in the Global South was only 2.4% of GDP on average, a quarter of the level recommended by the UN and a fraction of what rich countries spent.

Meanwhile, only 38% of the total went to social protection, with corporate loans and tax breaks getting the lion’s share.

Things will get worse unless there is a fundamental policy change. This year recovery funds have dried up and, as most countries are heavily indebted, the IMF projects large expenditure cuts.

In 2023, at least 94 developing countries are expected to cut public spending in terms of GDP. Our report estimates that 85% of the world’s population living in 143 countries will live in the grip of austerity measures by 2023, and the trend is likely to continue for years.

Unless these policies are reversed, people in developing countries will suffer as a result cuts to social protection and public services at a time they are most needed, with 3.3 billion people (or nearly half of mankind) expected to be living below the poverty line of US $5.50/day by the end of 2022.

This crisis will affect especially women who received half less COVID-19 recovery funds than their male counterparts.

But the impact goes far beyond women. Elderly pensioners and persons with disabilities will receive lower pension benefits. Workers around the world will see less job security, poorer pay and working conditions as regulations are dismantled.

A recent study on inequality found that the vast majority of countries were making labor markets more flexible to help big corporations. As inflation keeps rising, worsened by higher consumption taxes, families will be much affected while any support they receive will be less due to austerity cuts.

South Africa reflects the crisis of countries falling into the austerity trap. The government provided Social Relief of Distress (SRD) grants of R350 (US$24 in 2021) per month that were instituted at the start of the pandemic, supporting for the first-time low-income individuals who are of working age.

These grants have been extended several times, providing a lifeline for those worst hit by the pandemic.

However, despite the cost-of-living crisis, the government -advised by the IMF- is now considering reducing social expenditures and helping only the most vulnerable, leaving many low-income households without any support. Other austerity measures being discussed include cuts to the salaries of civil servants, and labor flexibilization reforms.

Instead of these austerity cuts, the South African government and the IMF should focus on raising additional revenues to fund social protection and public services, making sure everyone pays taxes, reducing corporate tax loopholes and exemptions, taxing excess profits and wealthy individuals.

Similarly, Ecuador has been shaken by social unrest because of austerity reforms. In 2019, after large riots, the government of Lenin Moreno flew from the capital and had to stop a loan with the IMF that had proposed cuts to subsidies and other austerity reforms.

In 2021, the same austerity policies were proposed again by the IMF, such as cuts to subsidies and public services, reducing social protection and labor regulations.

In 2022, farmers, indigenous men and women, marched again to the capital with pitchforks to join students and workers protesting austerity policies, forcing President Lasso to back down and agree to grant subsidies and other demands.

These are only two examples reflecting the austerity storm gathering around the world. This is extremely unfair and will generate unnecessary social hardship, as populations are struggling with a severe cost-of-living crisis, especially at a time when many countries are losing significant amounts of revenue to tax abuses, illicit financial flows and tax exemptions to large corporates that are wholly unnecessary.

Austerity cuts are not inevitable, there are alternatives even in the poorest countries. Instead of austerity cuts, governments can increase progressive tax revenues, restructure and eliminate debt, eradicate illicit financial flows, and re-allocate public expenditures, among other options.

Policy makers must act on this. All the human suffering and social unrest that austerity inflicts is unnecessary.

Civil society organizations have launched a global campaign to End Austerity, including, among others, ActionAid International, European Network on Debt and Development (Eurodad), Fight Inequality Alliance, Financial Transparency Coalition and Oxfam International.

Austerity campaign calls on citizens and organizations from all around the world to fight back against the wave of austerity sweeping the globe, supercharging inequality and compounding the effects of the cost-of-living crisis.

Our decision-makers need to wake up and change course. There is no time to lose.

Matti Kohonen is Executive Director of Financial Transparency Coalition; Isabel Ortiz is Director of the Global Social Justice Program at Joseph Stiglitz’s Initiative for Policy Dialogue

Opinion by Lars Jensen, George Gray Molina (united nations)

Inter Press Service

UNITED NATIONS, Oct 19 (IPS) – Developing low- and middle-income economies are taking hard hits from global economic developments outside their control. Monetary tightening in advanced economies coupled with increasing fears of a global recession have weakened currencies, sent interest rates soaring, and investors fleeing.

All of which is contributing to a rapid deterioration of an already damaging debt crisis which is, as ever, hitting the most vulnerable the hardest.

In new research released by the United Nations Development Programme (UNDP), 54 developing (low- and middle-income) economies are identified as suffering from severe debt problems, equal to 40 percent of all developing economies. 1

Providing this group of countries with the debt relief they need should be a manageable task for the international economy as the group only accounts for little more than 3% of the world economy. Failing to do so, however, could result in catastrophic development setbacks as the group of 54 accounts for more than 50 percent of the world’s extreme poor and 28 of the world’s top-50 most climate vulnerable countries.

Countries are stuck between a rock and a hard place. They cannot spend what is required to protect their citizens and safeguard their development prospects while continuing to also service their fast-rising debt burdens.

Time is running out. Without an urgent step-up of debt relief efforts from the international community, many more defaults will follow, and the debt crisis will turn into an entrenched development crisis as history has taught us.

Contrary to the advice given in the early stages of the COVID-19 pandemic, in the face of high interest rates, inflation, and debt levels, the International Monetary Fund is now urging countries to reign in fiscal spending while providing targeted and time-bound support to vulnerable populations.

But many developing economies cannot easily shift to effective and targeted social transfers or quickly increase tax revenues, – as the administrative capacity to do so takes years to build up.

Without a viable alternative in the form of access to orderly and comprehensive debt restructuring, and additional liquidity support from the international community, countries will have to choose between a string of messy and costly defaults and/or abrupt spending cuts with disastrous consequences for low-income and vulnerable populations and development prospects at large.

Furthermore, both options greatly increase the risk of political and social unrest threatening further setbacks and a deepening crisis.

We must also remember that these things are happening against the backdrop of an intensifying climate crisis which we can only combat together as a global community. Without a rethink on debt relief the global climate transition will be delayed, the economic costs of the transition will rise, and developing economies, who have contributed the least to the problem, will continue to bear a disproportionate size of the costs.

Developing economies must be allowed sufficient fiscal space to undertake ambitious sustainable development plans – including the undertaking of much-needed climate adaptation and mitigation investments.

Debt relief is one of several crucial components of providing it. The G20’s Common Framework for Debt Treatments, under which countries with debt distress can seek a restructuring, will have to be reformed, including a shift in focus towards comprehensive debt restructurings in return for sustainable development objectives.

This will require a change in attitude and sense of urgency, especially among major official creditors, as well as full debt transparency from both debtors and creditors. In our latest paper we discuss possible ways forward for the Common Framework focusing on country eligibility, debt sustainability analyses, official creditor coordination, private creditor participation, policy conditionalities and the use of debt clauses that target future economic and fiscal resilience.

Decisions on debt relief can no longer wait.

Nineteen developing economies – more than one-third of developing economies issuing dollar debt in international markets – have now lost markets access on account of skyrocketing interest rates, more than doubling from 9 countries at the beginning of 2022.

Similarly, credit ratings have been sliding with 27 countries – close to one-third of credit-rated developing economies – rated either ‘substantial risk, extremely speculative, or default’, up from 10 countries at the beginning of 2020.

Hard-won development gains achieved in the global south over decades are now being eroded by the intertwined cost-of-living and debt crises. Not only will a deepening development crisis result in great human suffering, but the cost of regaining whatever development gains are lost will increase substantially the longer we wait.

It is inconceivable, both morally and economically, that we would allow a development crisis to escalate when the international community has the resources needed to stop it now.

Lars Jensen is Economist at UNDP Strategic Policy Engagement Unit.; George Gray Molina is Head of Strategic Engagement and Chief Economist at UNDP

Opinion by Jomo Kwame Sundaram, Anis Chowdhury (sydney and kuala lumpur)

Inter Press Service

SYDNEY and KUALA LUMPUR, Oct 18 (IPS) – Preoccupied with enhancing their own ‘credibility’ and reputations, central banks (CBs) are again driving the world economy into recession, financial turmoil and debt crises.

Wall Street ‘cred’

Most CB governors believe ‘credibility’ is desirable and must be achieved by fighting inflation at any cost. To justify their own more harmful policies, they warn inflation is ‘damaging’.

Anis Chowdhury

They argue CBs need ‘independence’ from governments to pursue ‘credible’ monetary policy. Inflation targeting to ‘anchor’ inflation expectations is supposed to generate desired ‘confidence’. But CBs have been responsible for many costly failures.

The US Fed deepened the 1930s’ Great Depression, the 1970s’ stagflation and the early 1980s’ contraction, besides contributing to the 2008-09 global financial crisis (GFC). Hence, CB notions of ‘credibility’ and ‘independence’ need to be reconsidered.

But why did the Fed behave as it did? Some economic historians insist it was “to promote the interests of commercial banks, rather than economic recovery”.

Monetary policy before and during the Great Depression “was designed to cause the failure of non-member banks, which would enhance the long-run profits of the Fed’s member banks and enlarge the regulatory domain”.

Others concluded, “Federal Reserve errors seem largely attributable to the continued use of flawed policies” to defend the ‘gold standard’, and its poor understanding of monetary conditions.

Central banks contractionary

Worse, few lessons were learnt. Instead of protecting the gold standard, or being counter-cyclical, fighting inflation is the new CB preoccupation. Even worse, most CBs now commit to an arbitrarily-set inflation target of 2%, first promoted by the Reserve Bank of New Zealand over three decades ago.

Jomo Kwame Sundaram

Major CB interventions have caused both economic booms or bubbles and busts or contractions, often without mitigating inflation. Such “go-stop” monetary policy swings have caused asset price bubbles and financial fragility besides sudden contractions.

Ben Bernanke’s research team found the major damage from the 1970s’ oil price shocks was due to the “tightening of monetary policy” response. Other research attributed the 1970s’ stagflation largely to the Fed’s “go-stop” monetary policy, worsened by policymakers’ “misperceptions” and “faulty doctrine”.

Volcker’s actions betrayed the Fed’s dual mandate to pursue both full employment and price stability. First in the Employment Act of 1946, it was re-codified in the 1978 ‘Humphrey-Hawkins’ Full Employment and Balanced Growth Act.

The World Bank warns of dire developing country debt crises following policy-induced recessions. Meanwhile, the International Monetary Fund has warned developing economies with dollar-denominated debt of imminent foreign exchange crises.

Stop-go new norm

Fed, Bank of England and European Central Bank policy approaches still justify “go-stop” monetary policy reversals. Resulting booms or bubbles and busts also feature in other recent crises, e.g., the GFC.

CBs enabled credit expansion in the 2000s, culminating in the GFC. More worryingly, the “near-consensus view” is that independent CBs have failed to achieve – let alone protect – financial stability.

Easy credit and rising stock and housing markets have involved rapid credit and loan growth worsening asset price bubbles. Regulatory oversight became increasingly lax as investors ‘chased yield’. Leverage grew, using dodgy ‘derivative’ products, making proper risk assessment difficult.

Guy Debelle, once Deputy Governor of Australia’s CB, noted, “The goal of financial stability has generally been left vague”. Hence, CBs failed to see significant build-up of financial instability”. Soon after, the Lehman Brothers’ collapse precipitated the GFC.

With less investment in the real economy, supply capacity is falling behind still growing demand. Pandemic, war and sanctions have also disrupted supplies.

Raising interest rates, CBs now race to reverse earlier monetary expansion. Credit contractions are squeezing economies, hitting poorer countries especially hard.